Kenya’s Listed Banks FY'2025 Report, & Cytonn Weekly #15.2026

By Cytonn Research, Apr 19, 2026

Executive Summary

Fixed Income

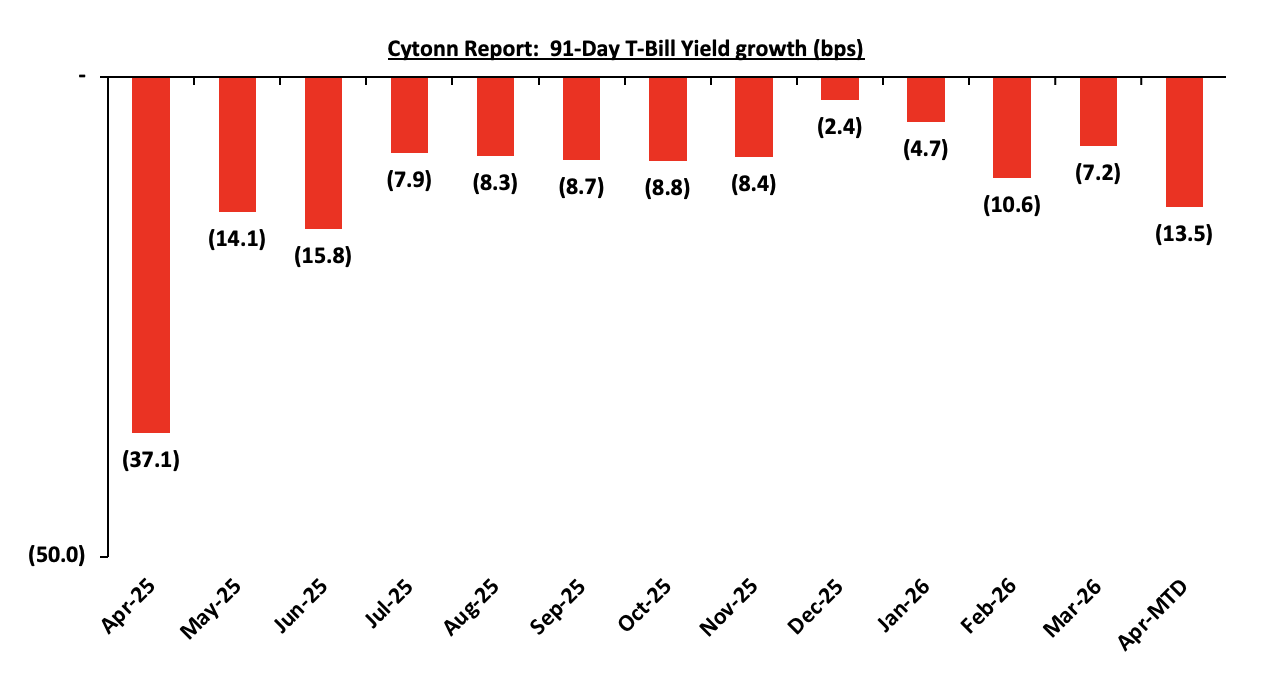

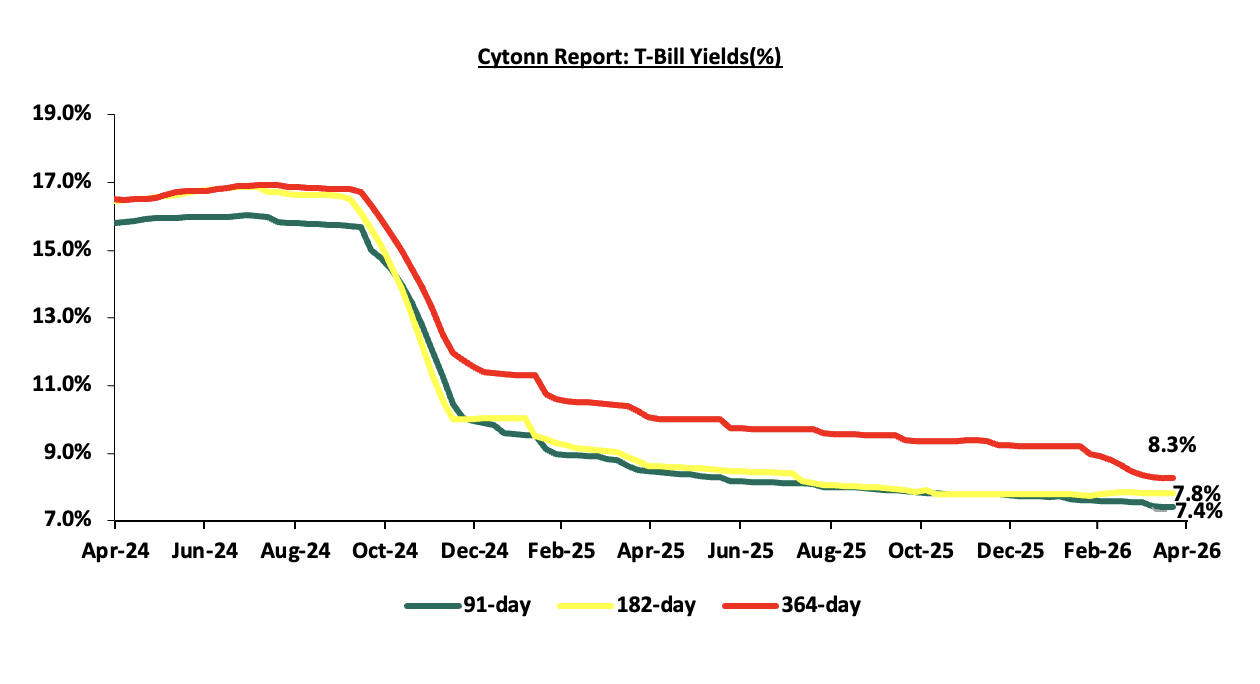

This week, T-bills were undersubscribed for the first time in two weeks, with the overall subscription rate coming in at 58.3%, lower than the subscription rate of 102.3% recorded the previous week. Investors’ preference for the shorter 91-day paper waned, with the paper receiving bids worth Kshs 2.6 bn against the offered Kshs 4.0 bn, translating to a subscription rate of 64.4%, significantly lower than the subscription rate of 199.4%, recorded the previous week. The subscription rate for the 182-day paper decreased to 76.7% from 108.5% recorded the previous week, while that of the 364-day paper decreased to 37.5% from 57.2% recorded the previous week. The government accepted a total of Kshs 13.97 bn worth of bids out of Kshs 14.0 bn bids received, translating to an acceptance rate of 99.8%. The yields on the government papers were on an upward trajectory with the yields on the 91-day, 364-day and 182-day papers increasing by 2.4 bps, 0.2 bps and 0.02 bps but remained at 7.4%, 8.3% and 7.8% recorded the previous week respectively;

During the week, the Central Bank of Kenya released the auction results for the switch of treasury bonds from FXD1/2016/01, with a tenor to maturity of 0.3 years and a fixed coupon rate of 15.0%, to FXD1/2018/015, a with a tenor to maturity of 7.1 years and a fixed coupon rate of 12.7%. This marks the third bond switch this year, following the switches to FXD1/2022/015, and FXD3/2019/015 in January 2026, and March 2026 respectively. The bond was undersubscribed, with the overall subscription rate coming in at 12.8%, receiving bids worth Kshs 2.6 bn against the offered Kshs 20.0 bn. The government accepted bids worth Kshs 1.8 bn, translating to an acceptance rate of 68.5%. The weighted average yield for the accepted bids for the FXD1/2018/015 came in at 12.0%. With the Inflation rate at 4.4% as of March 2026, the real return of the FXD1/2018/015 was 7.6%. Given the 10.0% withholding tax on the bonds, the tax equivalent yields for shorter term bonds with 15.0% withholding tax is 14.1% for the FXD1/2018/015;

During the week, the Central Bank of Kenya released the auction results for the re-opened treasury bond SDB1/2011/030 and the new treasury bond issue FXD1/2026/030 with tenors to maturities of 14.9 years and 30.0 years respectively and fixed coupon rates of 12.0% and 12.5% respectively. The bonds were oversubscribed, with the overall subscription rate coming in at 191.7%, receiving bids worth Kshs 38.3 bn against the offered Kshs 20.0 bn. The government accepted bids worth Kshs 30.1 bn, translating to an acceptance rate of 78.4%. The weighted average yield for the accepted bids for the SDB1/2011/030 and FXD1/2026/030 came in at 13.0% and 13.8% respectively. Notably, the 13.0% yield on SDB1/2011/030 was lower than the 13.3% recorded at its last reopening in December 2025. With the Inflation rate at 4.4% as of March 2026, the real returns of the SDB1/2011/030 and FXD1/2026/030 are 8.6% and 9.4%. Given the 10.0% withholding tax on the bonds, the tax equivalent yields for shorter term bonds with 15.0% withholding tax are 12.7% and 13.2% for the SDB1/2011/030 and FXD1/2026/030 respectively;

During the week, The Energy and Petroleum Regulatory Authority (EPRA) released their monthly statement on the maximum retail fuel prices in Kenya, effective from 15th April 2026 to 14th May 2026. Notably, the maximum allowed prices for Super Petrol, and Diesel increased by Kshs 28.7, and Kshs 40.3 per litre to Kshs 207.0, and Kshs 206.8 per litre from Kshs 178.3, and Kshs 166.5 per litre respectively in March 2026, marking the first increase in 2026. On the other hand, Kerosene remained unchanged at Kshs 152.8 per litre. Following a further review, the Authority issued a revised pricing schedule effective 16th April 2026 to 14th May 2026, in which Super Petrol and Diesel prices were adjusted downwards by Kshs 9.4 and Kshs 10.2 per litre to Kshs 197.6 and Kshs 196.6 per litre respectively, while Kerosene remained unchanged at Kshs 152.8 per litre;

The National Treasury gazetted the revenue and net expenditures for the ninth month of FY’2025/2026, ending 31st March 2026, highlighting that the total revenue collected as at the end of March 2026 amounted to Kshs 1,833.3 bn, equivalent to 65.8% of the revised estimates of Kshs 2,784.4 bn for FY’2025/2026 and is 87.8% of the prorated estimates of Kshs 2,088.3 bn.

Equities

During the week, the equities market was on an upward trajectory with al the indices increasing ,the NASI gained the most by 0.5%, while NSE 20, NSE 25, and NSE 10 gained by 0.5%, 0.2% and 0.1% respectively, taking the YTD performance to gains of 14.8%, 12.5%, 11.1% and 10.0% for NSE 20, NSE 25, NASI and NSE 10 respectively. The equities market performance was mainly driven by gains recorded by large cap stocks such as Co-operative Bank, Standard Chartered, and Stanbic of 5.2%, 4.7% and 3.0% respectively. However, the performance was weighed down by losses recorded by large cap stocks such as KCB, EABL and DTB-K of 2.5%, 1.0% and 0.7% respectively;

Also, during the week, the banking sector index gained by 1.0% to 241.1 from 238.9 recorded the previous week. This is attributable to gains recorded by stocks such as Co-operative Bank, Standard Chartered, and Stanbic of 5.2%, 4.7% and 3.0% respectively. However, the performance was weighed down by losses recorded by large cap stocks such as KCB, DTB-K and NCBA of 2.5%, 0.7% and 0.3% respectively;

Real Estate

During the week, the World Bank approved Kshs 71.0 bn (USD 550.0 mn) in financing for the upgrade of the Nairobi–Mandera road corridor, marking a significant infrastructure investment under the Horn of Africa Gateway Development Project. The funding will be disbursed in two tranches, including USD 290.0 mn for the additional financing phase and USD 260.0 mn for the second phase of the program. The project targets the upgrade of approximately 508.0 km of the Isiolo–Mandera corridor, alongside the installation of about 1,270.0 km of high-capacity fibre optic infrastructure, aimed at enhancing both transport and digital connectivity in Northern Kenya;

During the week, The Government, in partnership with UNEP and UN Habitat announced Nairobi as the focus of a new Kshs 672.0 mn urban greening initiative aimed at transforming parts of the city into greener and more climate-resilient spaces. The programme is expected to target areas including Kamukunji as a pilot “green neighborhood,” with plans to improve urban environmental conditions and public spaces for residents;

During the week, the High Court halted the construction of a disputed affordable housing project in Githunguri, Kiambu County, following a legal challenge over the development of 2,180 housing units on the site. The ruling stopped ongoing works as the matter awaits full determination by the court;

During the week, Singapore-based lodging operator The Ascott Limited announced a partnership with Kenyan insurer Britam Holdings to develop a new 160-room hotel in Nairobi’s Kilimani area. The project, branded Citadines Westview Nairobi, will be located adjacent to the existing Somerset Westview Nairobi serviced apartments and is scheduled to open in early 2028. The development is structured as a dual-brand hospitality offering targeting both short-stay and extended-stay guests, and is expected to include hotel rooms, studios, and one-bedroom apartments;

During the week, Laptrust released the FY’2025 financial results for the Imara I-REIT for the period ended 31st December 2025. I-REIT holds several properties across the country including; Pension towers, CPF House, Metro Park, Freedom Heights mall, Freedom Heights serviced plot, Man apartments, and Nova Pioneer in Eldoret. The basic earnings per unit came in at Kshs (0.8) in FY’2025, a 37.2% decline from Kshs (0.6) recorded in FY’2024. The performance was driven by a 37.2% increase in net losses to Kshs 280.3 mn in FY’2025 from Kshs 204.3 mn recorded in FY’2024;

On the Unquoted Securities Platform Acorn D-REIT and I-REIT traded at Kshs 27.4 and Kshs 23.2per unit, respectively, as per the last updated data on 10th April 2026. The performance represented a 33.4% and 14.5% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. The volumes traded for the D-REIT and I-REIT came in at 13.4 mn and 42.2 mn shares, respectively. Additionally, ILAM Fahari I-REIT traded at Kshs 13.8 per share as of 10th April 2026, representing a 31.0% loss from the Kshs 20.0 inception price;

Focus of the Week

Following the release of the FY’2025 results by Kenyan listed banks, the Cytonn Financial Services Research Team undertook an analysis on the financial performance of the listed banks and identified the key factors that shaped the performance of the sector;

Investment Updates:

- Weekly Rates:

- Cytonn Money Market Fund closed the week at a yield of 11.23% p.a. To invest, dial *809# or download the Cytonn App from Google Play store here or from the Appstore here;

- We continue to offer Wealth Management Training every Tuesday, from 7:00 pm to 8:00 pm. The training aims to grow financial literacy among the general public. To register for any of our Wealth Management Trainings, click here;

- If interested in our Private Wealth Management Training for your employees or investment group, please get in touch with us through wmt@cytonn.com;

- Cytonn Insurance Agency acts as an intermediary for those looking to secure their assets and loved ones’ future through insurance namely; Motor, Medical, Life, Property, WIBA, Credit and Fire and Burglary insurance covers. For assistance, get in touch with us through insuranceagency@cytonn.com;

- Cytonn Asset Managers Limited (CAML) continues to offer pension products to meet the needs of both individual clients who want to save for their retirement during their working years and Institutional clients that want to contribute on behalf of their employees to help them build their retirement pot. To more about our pension schemes, kindly get in touch with us through pensions@cytonn.com;

Hospitality Updates:

- We currently have promotions for Staycations. Visit cysuites.com/offers for details or email us at sales@cysuites.com;

Money Markets, T-Bills Primary Auction:

This week, T-bills were undersubscribed for the first time in two weeks, with the overall subscription rate coming in at 58.3%, lower than the subscription rate of 102.3% recorded the previous week. Investors’ preference for the shorter 91-day paper waned, with the paper receiving bids worth Kshs 2.6 bn against the offered Kshs 4.0 bn, translating to a subscription rate of 64.4%, significantly lower than the subscription rate of 199.4%, recorded the previous week. The subscription rate for the 182-day paper decreased to 76.7% from 108.5% recorded the previous week, while that of the 364-day paper decreased to 37.5% from 57.2% recorded the previous week. The government accepted a total of Kshs 13.97 bn worth of bids out of Kshs 14.0 bn bids received, translating to an acceptance rate of 99.8%. The yields on the government papers were on an upward trajectory with the yields on the 91-day, 364-day and 182-day papers increasing by 2.4 bps, 0.2 bps and 0.02 bps to remain relatively unchanged from the 7.4%, 8.3% and 7.8% recorded the previous week respectively.

The chart below shows the yield growth rate for the 91-day paper from April 2025 to date:

The chart below shows the performance of the 91-day, 182-day and 364-day papers from April 2024 to April 2026:

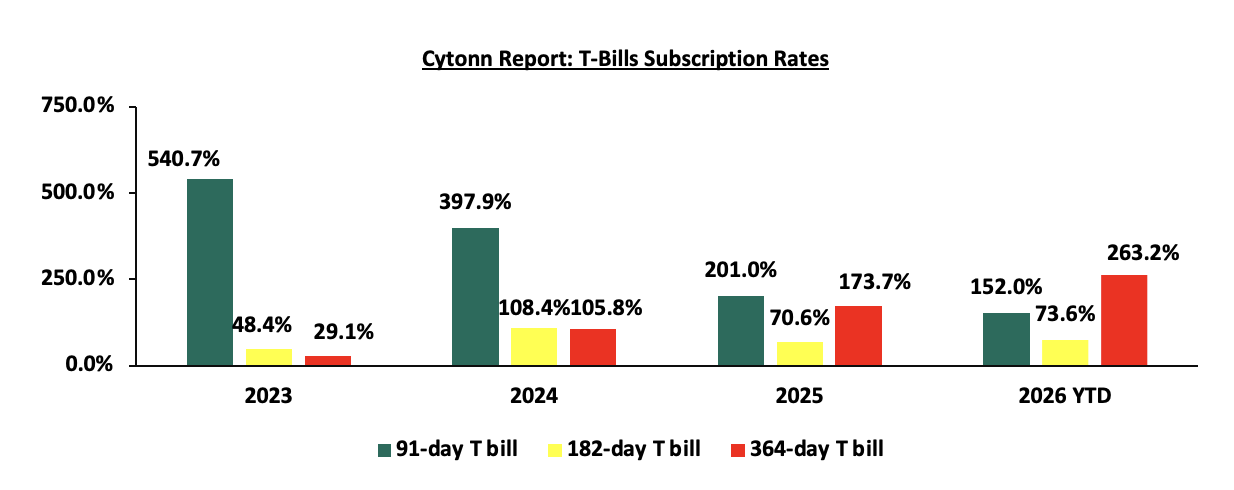

The chart below compares the overall average T-bill subscription rates obtained in 2023, 2024, 2025 and 2026 Year-to-date (YTD):

T-Bonds Primary Auction:

During the week, the Central Bank of Kenya released the auction results for the switch of treasury bonds from FXD1/2016/01, with a tenor to maturity of 0.3 years and a fixed coupon rate of 15.0%, to FXD1/2018/015, a with a tenor to maturity of 7.1 years and a fixed coupon rate of 12.7%. This marks the third bond switch this year, following the switches to FXD1/2022/015, and FXD3/2019/015 in January 2026, and March 2026 respectively. The bond was undersubscribed, with the overall subscription rate coming in at 12.8%, receiving bids worth Kshs 2.6 bn against the offered Kshs 20.0 bn. The government accepted bids worth Kshs 1.8 bn, translating to an acceptance rate of 68.5%. The weighted average yield for the accepted bids for the FXD1/2018/015 came in at 12.0%. With the Inflation rate at 4.4% as of March 2026, the real return of the FXD1/2018/015 was 7.6%. Given the 10.0% withholding tax on the bonds, the tax equivalent yields for shorter term bonds with 15.0% withholding tax is 14.1% for the FXD1/2018/015.

During the week, the Central Bank of Kenya released the auction results for the re-opened treasury bond SDB1/2011/030 and the new treasury bond issue FXD1/2026/030 with tenors to maturities of 14.9 years and 30.0 years respectively and fixed coupon rates of 12.0% and 12.5% respectively. The bonds were oversubscribed, with the overall subscription rate coming in at 191.7%, receiving bids worth Kshs 38.3 bn against the offered Kshs 20.0 bn. The government accepted bids worth Kshs 30.1 bn, translating to an acceptance rate of 78.4%. The weighted average yield for the accepted bids for the SDB1/2011/030 and FXD1/2026/030 came in at 13.0% and 13.8% respectively. Notably, the 13.0% yield on SDB1/2011/030 was lower than the 13.3% recorded at its last reopening in December 2025. With the Inflation rate at 4.4% as of March 2026, the real returns of the SDB1/2011/030 and FXD1/2026/030 are 8.6% and 9.4%. Given the 10.0% withholding tax on the bonds, the tax equivalent yields for shorter term bonds with 15.0% withholding tax are 12.7% and 13.2% for the SDB1/2011/030 and FXD1/2026/030 respectively.

Money Market Performance:

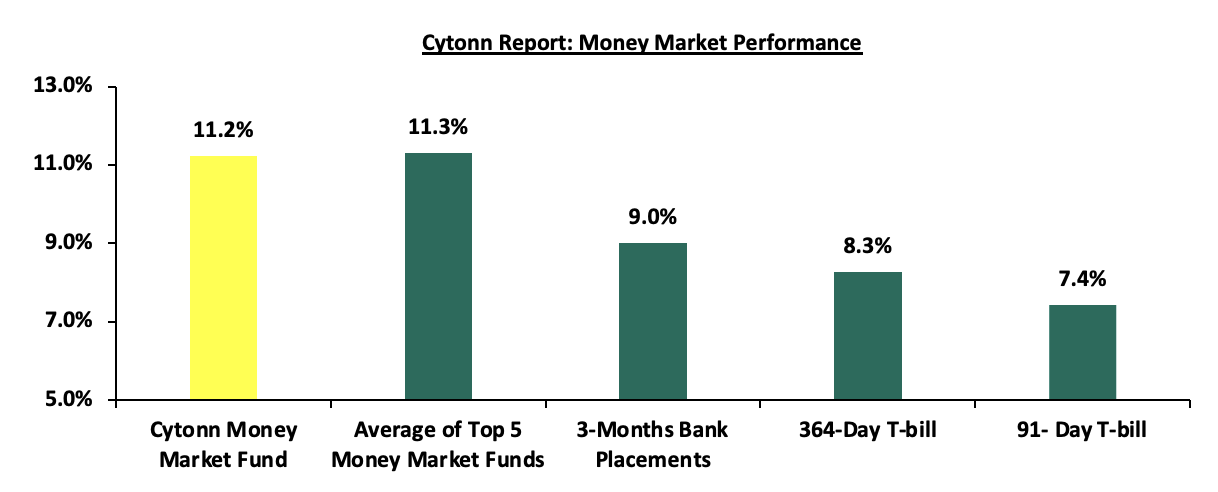

In the money markets, 3-month bank placements ended the week at 9.0% (based on rates offered by various banks). The yields on the government papers were on an upward trajectory with the yields on the 91-day, and 364-day papers increasing by 2.4 bps and 0.2 bps to remain relatively unchanged from the 7.4%, and 8.3% recorded the previous week respectively. The yield on the Cytonn Money Market Fund increased by 3.0 bps to remain relatively unchanged at 11.2% recorded the previous week, while the average yields on the Top 5 Money Market Funds decreased by 19.2 bps to 11.3% from 11.5% recorded the previous week.

The table below shows the Money Market Fund Yields for Kenyan Fund Managers as published on 17th April 2026:

|

Money Market Fund Yield for Fund Managers as published on 17th April 2026 |

||

|

Rank |

Fund Manager |

Effective Annual Rate |

|

1 |

Etica Money Market Fund |

11.9% |

|

2 |

Nabo Africa Money Market Fund |

11.6% |

|

3 |

Cytonn Money Market Fund (Dial *809# or download Cytonn App) |

11.2% |

|

4 |

Arvocap Money Market Fund |

11.0% |

|

5 |

Gulfcap Money Market Fund |

10.8% |

|

6 |

Enwealth Money Market Fund |

10.6% |

|

7 |

Lofty-Corban Money Market Fund |

10.6% |

|

8 |

Ndovu Money Market Fund |

10.5% |

|

9 |

Jubilee Money Market Fund |

10.4% |

|

10 |

Orient Kasha Money Market Fund |

10.3% |

|

11 |

Madison Money Market Fund |

10.3% |

|

12 |

Kuza Money Market fund |

10.2% |

|

13 |

Faulu Money Market Fund |

10.1% |

|

14 |

Old Mutual Money Market Fund |

10.1% |

|

15 |

GenAfrica Money Market Fund |

9.7% |

|

16 |

British-American Money Market Fund |

9.5% |

|

17 |

Dry Associates Money Market Fund |

9.3% |

|

18 |

Apollo Money Market Fund |

9.3% |

|

20 |

SanlamAllianz Money Market Fund |

9.1% |

|

21 |

KCB Money Market Fund |

9.0% |

|

22 |

Genghis Money Market Fund |

8.7% |

|

23 |

CIC Money Market Fund |

8.4% |

|

24 |

ICEA Lion Money Market Fund |

8.3% |

|

25 |

Co-op Money Market Fund |

8.3% |

|

26 |

CPF Money Market Fund |

8.2% |

|

27 |

Mali Money Market Fund |

8.0% |

|

28 |

Mayfair Money Market Fund |

7.6% |

|

29 |

Absa Shilling Money Market Fund |

7.4% |

|

30 |

Ziidi Money Market Fund |

6.0% |

|

31 |

AA Kenya Shillings Fund |

5.9% |

|

32 |

Stanbic Money Market Fund |

5.4% |

|

33 |

Equity Money Market Fund |

4.3% |

Source: Business Daily

Liquidity:

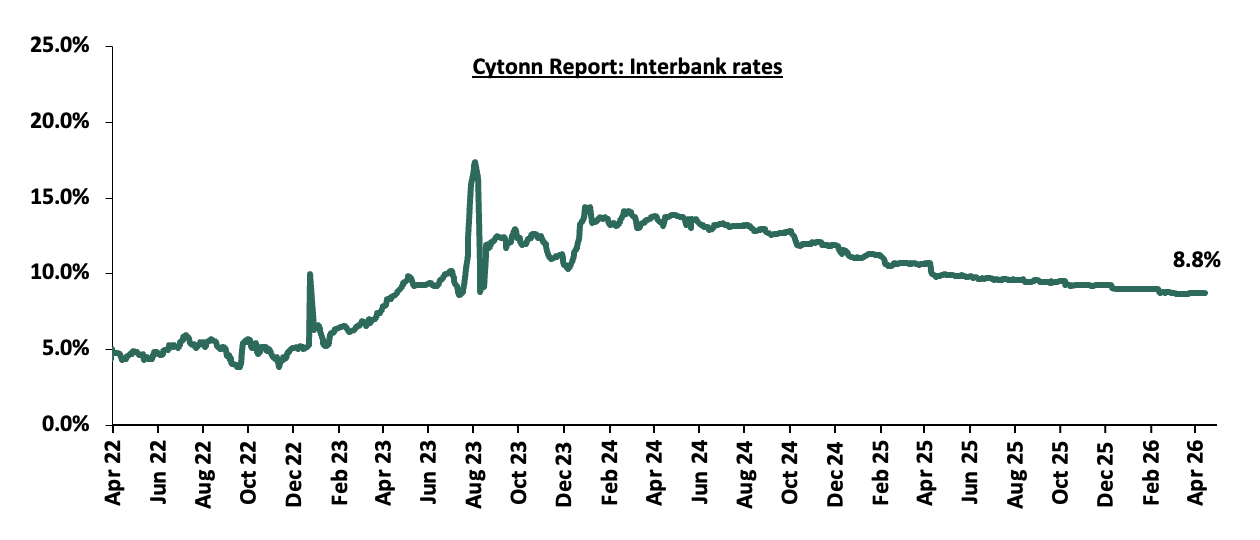

During the week, liquidity in the money markets tightened with the average interbank rate increasing by 0.5 bps to remain relatively unchanged at 8.8% recorded last week, partly attributable to tax remittances that offset government payments. The average interbank volumes traded decreased by 20.2% to Kshs 11.2 bn from Kshs 14.0 bn recorded the previous week. The chart below shows the interbank rates in the market over the years:

Kenya Eurobonds:

During the week, the yields on the Eurobonds were on a downward trajectory with the yield on the 7-year Eurobond issued in 2024, decreasing the most by 35.0 bps to 8.1% from 8.5% recorded the previous week. The table below shows the summary performance of the Kenyan Eurobonds as of 16th April 2026;

|

Cytonn Report: Kenya Eurobonds Performance |

||||||

|

|

2018 |

2019 |

2021 |

2024 |

||

|

Tenor |

10-year issue |

30-year issue |

12-year issue |

13-year issue |

7-year issue |

|

|

Amount Issued (USD) |

1.0 bn |

1.0 bn |

1.0 bn |

1.5 bn |

1.5 bn |

|

|

Years to Maturity |

2.5 |

22.5 |

8.8 |

5.5 |

10.5 |

|

|

Yields at Issue |

7.3% |

8.3% |

6.2% |

10.4% |

9.9% |

|

|

02-Jan-26 |

6.1% |

8.8% |

7.2% |

7.8% |

7.1% |

|

|

01-Apr-26 |

7.6% |

9.5% |

8.7% |

9.2% |

8.8% |

|

|

09-Apr-26 |

7.5% |

9.2% |

8.3% |

8.7% |

8.5% |

|

|

10-Apr-26 |

7.3% |

9.0% |

8.2% |

8.5% |

8.2% |

|

|

13-Apr-26 |

7.3% |

9.1% |

8.2% |

8.5% |

8.2% |

|

|

14-Apr-26 |

7.2% |

8.9% |

7.9% |

8.2% |

7.9% |

|

|

15-Apr-26 |

7.2% |

8.9% |

7.9% |

8.3% |

7.9% |

|

|

16-Apr-26 |

7.3% |

9.1% |

8.1% |

8.5% |

8.1% |

|

|

Weekly Change |

(0.2%) |

(0.1%) |

(0.2%) |

(0.1%) |

(0.3%) |

|

|

MTD Change |

(0.3%) |

(0.4%) |

(0.6%) |

(0.7%) |

(0.7%) |

|

|

YTD Change |

1.3% |

0.2% |

0.7% |

0.4% |

0.8% |

|

Source: Central Bank of Kenya (CBK) and National Treasury

Kenya Shilling:

During the week, the Kenya Shilling appreciated by 3.1 bps against the US Dollar, to Kshs 129.1 from the Kshs 129.2 recorded the previous week. On a year-to-date basis, the shilling has depreciated by 4.6 bps against the dollar, as compared to the 22.9 bps appreciation recorded in 2025.

We expect the shilling to be supported by:

- Diaspora remittances standing at a cumulative USD 5,051.2 mn in the twelve months to February 2026, 1.9% higher than the USD 4,956.5 mn recorded over the same period in 2025. These have continued to cushion the shilling against further depreciation. In the February 2026 diaspora remittances figures, North America remained the largest source of remittances to Kenya accounting for 54.2% in the period, and,

- Tourism inflows, which strengthened significantly. Tourism receipts reached Kshs 560.0 bn in 2025, up from Kshs 452.2 bn in 2024, representing a 23.9% increase, supported by improved international arrivals through the country’s major airports, and,

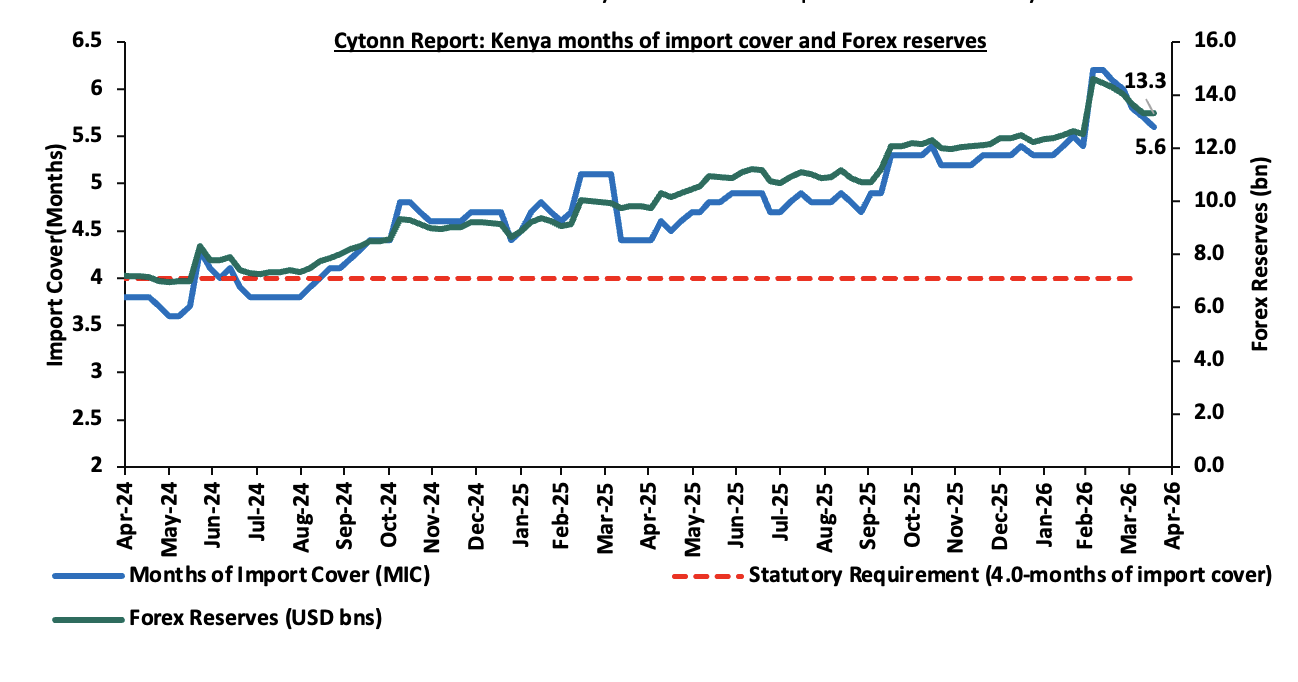

- Improved forex reserves currently at USD 13.3 bn (equivalent to 5.6-months of import cover), which is above the statutory requirement of maintaining at least 4.0-months of import cover and above the EAC region’s convergence criteria of 4.5-months of import cover.

The shilling is however expected to remain under pressure in 2026 as a result of:

- An ever-present current account deficit which came at 2.4% of GDP in the twelve months to February 2026, and,

- The need for government debt servicing, continues to put pressure on forex reserves given that 52.0% of Kenya’s external debt is US Dollar-denominated as of September 2025.

- Rising geopolitical tensions in the Middle East, which could exert pressure on the shilling through higher global oil prices and increased uncertainty in international markets. Given that Kenya is a net importer of petroleum products, any sustained increase in oil prices would widen the import bill, increase demand for US Dollars, and consequently put depreciation pressure on the shilling..

Kenya’s forex reserves decreased by 0.1% during the week to remain relatively unchanged at USD 13.3 bn recorded the previous week, equivalent to 5.6 months of import cover, and above the statutory requirement of maintaining at least 4.0-months of import cover.

The chart below summarizes the evolution of Kenya's months of import cover over the years:

Weekly Highlights

- Fuel Prices effective 16th April – 14th May 2026

During the week, The Energy and Petroleum Regulatory Authority (EPRA) released their monthly statement on the maximum retail fuel prices in Kenya, effective from 15th April 2026 to 14th May 2026. Notably, the maximum allowed prices for Super Petrol, and Diesel increased by Kshs 28.7, and Kshs 40.3 per litre to Kshs 207.0, and Kshs 206.8 per litre from Kshs 178.3, and Kshs 166.5 per litre respectively in March 2026, marking the first increase in 2026. On the other hand, Kerosene remain unchanged at Kshs 152.8 per litre. Subsequently, the Authority issued a revised pricing schedule effective 16th April 2026 to 14th May 2026, in which Super Petrol and Diesel prices were adjusted downwards by Kshs 9.4 and Kshs 10.2 per litre to Kshs 197.6 and Kshs 196.6 per litre respectively, while Kerosene remained unchanged at Kshs 152.8 per litre.

Other key take-outs from the performance include,

- The average landing cost per cubic metre of Kerosene, Diesel, and Super Petrol increased by 105.2%, 68.7% and 41.5% to USD 1,311.9, USD 1,073.2 and USD 823.9 in March 2026 from USD 639.5, USD 636.5 and USD 582.1 recorded in February 2026.

- The Kenyan Shilling depreciated against the US Dollar by 54.1 bps to Kshs 130.1 in March from 129.4 recorded in February

- The government reduced Value Added Tax (VAT) on petroleum products to 13% from 16% and later amended the VAT to 8% from 13% in the April 2026 pricing cycle, aimed at cushioning consumers from the sharp increase in global oil prices.

- The government reduced the level of price stabilization on Kerosene, Diesel and Super Petrol to Kshs 89.4, Kshs 22.2 and 4.3 Kshs per litre in the revised release from Kshs 108.1, Kshs 23.9 and Kshs 4.7 per litre in the original release respectively.

We note that while fuel prices have seen a sharp upward adjustment in the April 2026 cycle, the government’s continued intervention through the price stabilization mechanism, with the government planning to utilize approximately Kshs 6.2 bn of the Petroleum Development Levy (PDL) Fund to stabilize the prices and a stable Kenyan Shilling have prevented even steeper increases. Without these efforts, the record surges in landing costs for Kerosene, Diesel and Super Petrol, would have dealt a far more severe blow to the economy.

Going forward, the outlook for fuel prices remains cautious. While the government's stabilization framework provides a cushion, persistent geopolitical tensions in the Middle East suggest that global oil prices may remain volatile. Given Diesel’s role as a key input in production and transportation, the recent prices increase is expected to exert cost-push pressures across sectors, particularly in manufacturing, agriculture, and logistics, triggering a sharp rise in transportation costs and fueling broader inflationary pressures as these added expenses are passed down to the final consumer. However, provided the exchange rate remains firm and the Petroleum Development Levy remains active, we anticipate that inflationary pressures will be managed, keeping the overall rate broadly within the Central Bank of Kenya’s preferred target range of 2.5% - 7.5% in the medium term.

- Exchequer Highlight January 2026

The National Treasury gazetted the revenue and net expenditures for the ninth month of FY’2025/2026, ending 31st March 2026, highlighting that the total revenue collected as at the end of March 2026 amounted to Kshs 1,833.3 bn, equivalent to 65.8% of the revised estimates of Kshs 2,784.4 bn for FY’2025/2026 and is 87.8% of the prorated estimates of Kshs 2,088.3 bn. Below is a summary of the performance:

|

FY'2025/2026 Budget Outturn - As at 31st March 2026 |

||||||

|

Amounts in Kshs billions unless stated otherwise |

||||||

|

Item |

12-months Original Estimates |

Revised Estimates |

Actual Receipts/Release |

Percentage Achieved |

Prorated |

% achieved of the Prorated |

|

Opening Balance |

|

|

6.4 |

|

|

|

|

Tax Revenue |

2,627.1 |

2,600.8 |

1,717.6 |

66.0% |

1,950.6 |

88.1% |

|

Non-Tax Revenue |

127.6 |

183.6 |

109.3 |

59.5% |

137.7 |

79.3% |

|

Total Revenue |

2,754.7 |

2,784.4 |

1,833.3 |

65.8% |

2,088.3 |

87.8% |

|

External Loans & Grants |

569.8 |

694.3 |

553.4 |

79.7% |

520.7 |

106.3% |

|

Domestic Borrowings |

1,098.3 |

1,669.7 |

965.9 |

57.8% |

1,252.3 |

77.1% |

|

Other Domestic Financing |

10.8 |

10.8 |

8.2 |

75.6% |

8.1 |

100.8% |

|

Total Financing |

1,678.9 |

2,374.8 |

1,527.4 |

64.3% |

1,781.1 |

85.8% |

|

Recurrent Exchequer issues |

1,470.4 |

1,676.6 |

1,171.9 |

69.9% |

1,257.4 |

93.2% |

|

CFS Exchequer Issues |

2,141.0 |

2,584.6 |

1,496.7 |

57.9% |

1,938.5 |

77.2% |

|

Development Expenditure & Net Lending |

407.1 |

483.0 |

262.6 |

54.4% |

362.2 |

72.5% |

|

County Governments + Contingencies |

415.0 |

415.0 |

276.0 |

66.5% |

311.3 |

88.7% |

|

Total Expenditure |

4,433.6 |

5,159.2 |

3,207.2 |

72.3% |

2,955.7 |

108.5% |

|

Fiscal Deficit excluding Grants |

1,678.9 |

2,374.8 |

1,373.9 |

57.9% |

1,781.1 |

77.1% |

|

Total Borrowing |

1,668.1 |

2,364.0 |

1,519.2 |

64.3% |

1,773.0 |

85.7% |

The key take-outs from the release include;

- Total revenue collected as at the end of February 2026 amounted to Kshs 1,833.3 bn, equivalent to 65.8% of the revised estimates of Kshs 2,784.4 bn for FY’2025/2026 and is 87.8% of the prorated estimates of Kshs 2,088.3 bn. Cumulatively, tax revenues amounted to Kshs 1,717.6 bn, equivalent to 66.0% of the revised estimates of Kshs 2,600.8 bn and 88.1% of the prorated estimates of Kshs 1,950.6 bn,

- Total financing amounted to Kshs 1,527.4 bn, equivalent to 64.3% of the revised estimates of Kshs 2,374.8 bn and is equivalent to 85.8% of the prorated estimates of Kshs 1,781.1 bn. Additionally, domestic borrowing amounted to Kshs 965.9 bn, equivalent to 57.8% of the revised estimates of Kshs 1,669.7 bn and is 77.1% of the prorated estimates of Kshs 1,252.3 bn.

- The total expenditure amounted to Kshs 3,207.2 bn, equivalent to 72.3% of the revised estimates of Kshs 5,159.2 bn, and is 108.5% of the prorated target expenditure estimates of Kshs 2,955.7 bn. Additionally, the net disbursements to recurrent expenditures came in at Kshs 1,171.9 bn, equivalent to 69.9% of the revised estimates of Kshs 1,676.6 and are equivalent to 93.2% of the prorated estimates of Kshs 1,257.4bn,

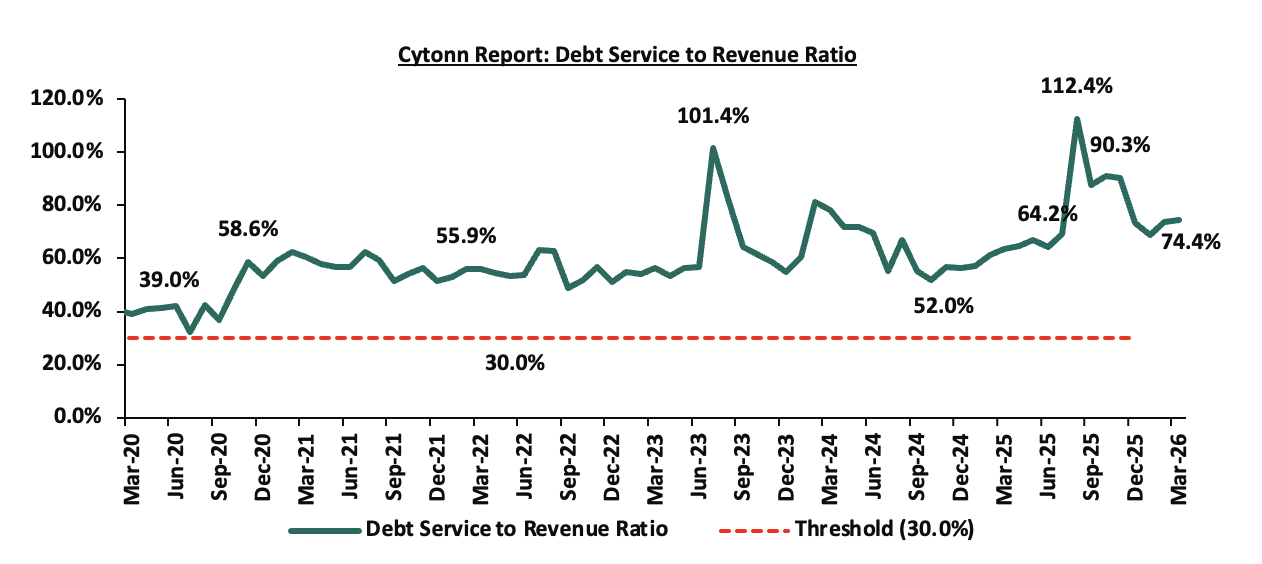

- Consolidated Fund Services (CFS) Exchequer issues came in at Kshs 1,496.7 bn, equivalent to 57.9% of the revised estimates of Kshs 2,584.6 bn, and are 77.2% of the prorated amount of Kshs 1,938.5 bn. The cumulative public debt servicing cost amounted to Kshs 1,364.7 bn which is 58.2% of the revised estimates of Kshs 2,344.6 bn and is 77.6% of the prorated estimates of Kshs 1,758.4 bn. Additionally, the Kshs 1,364.7 bn debt servicing cost is equivalent to 74.4% of the actual cumulative revenues collected as at the end of March 2026. The chart below shows the debt servicing cost to revenue ratio over the period;

- Total borrowings as at the end of February 2026 amounted to Kshs 1,519.2 bn, equivalent to 64.3% of the revised estimates of Kshs 2,364.0 bn for FY’2025/2026 and are 85.7% of the prorated estimates of Kshs 1,773.0 bn. The cumulative domestic borrowing of Kshs 1,669.7 bn comprises of Net Domestic Borrowing Kshs 1,125.4 bn and Internal Debt Redemptions (Rollovers) Kshs 544.3 bn.

The government underachieved its prorated revenue targets for the ninth month of the FY’2025/2026, achieving 87.8% of the prorated revenue targets in March 2026, similar February 2026. This was driven by shortfall in tax revenues and non-tax revenues, which stood at 88.1% and 79.3% of prorated levels respectively, with collections amounting to Kshs 1,171.6 bn in tax revenue and Kshs 109.3 bn in non-tax revenue. External loans and grants were ahead target at 106.3%, reducing reliance on domestic borrowing, which came in at 77.1% of the prorated target of Kshs 520.7 bn. The business environment, however, showed signs of deterioration, with the Purchasing Managers’ Index (PMI) standing at 47.4 in March 2026 despite dropping from 50.4 in February 2026, falling below the 50.0 neutral mark and signaling a contraction of business activity. Expenditure absorption stood at 108.5% of prorated levels, with development spending still lagging at 72.5%, reflecting slow implementation of capital projects. Future revenue performance will depend on how quickly private sector activity strengthens, supported by a stable Shilling, easing credit conditions following the decision to maintain the Central Bank Rate at 8.75% in April 2026, and continued efforts to broaden the tax base, curb evasion, and stimulate economic growth. However, the outlook remains vulnerable to external shocks, particularly the ongoing Iran-Israel conflict, which has heightened global oil price volatility and supply chain disruptions, posing upside risks to inflation and production costs, and potentially constraining private sector expansion and revenue mobilization.

Rates in the Fixed Income market have been on a downward trend due to high liquidity in the money market which allowed the government to front load most of its borrowing. The government is 96.9% ahead of its prorated net domestic borrowing target of Kshs 634.8 bn, having a net borrowing position of Kshs 1,006.1 bn (inclusive of T-bills). However, we expect a stabilization of the yield curve in the short and medium term, with the government looking to increase its external borrowing to maintain the fiscal surplus, hence alleviating pressure in the domestic market. As such, we expect the yield curve to stabilize in the short to medium-term and hence investors are expected to shift towards the long-term papers to lock in the high returns.

Market Performance:

During the week, the equities market was on an upward trajectory, with NASI gaining the most by 0.5%, while NSE 20, NSE 25, and NSE 10 gained by 0.5%, 0.2% and 0.1% respectively, taking the YTD performance to gains of 14.8%, 12.5%, 11.1% and 10.0% for NSE 20, NSE 25, NASI and NSE 10 respectively. The equities market performance was mainly driven by gains recorded by large cap stocks such as Co-operative Bank, Standard Chartered, and Stanbic of 5.2%, 4.7% and 3.0% respectively. However, the performance was weighed down by losses recorded by large cap stocks such as KCB, EABL and DTB-K of 2.5%, 1.0% and 0.7% respectively.

Also, during the week, the banking sector index gained by 1.0% to 241.1 from 238.9 recorded the previous week. This is attributable to gains recorded by stocks such as Co-operative Bank, Standard Chartered, and Stanbic of 5.2%, 4.7% and 3.0% respectively. However, the performance was weighed down by losses recorded by large cap stocks such as KCB, DTB-K and NCBA of 2.5%, 0.7% and 0.3% respectively;

During the week, equities turnover increased by 95.4% to USD 41.7 mn from USD 21.3 mn recorded the previous week, taking the YTD total turnover to USD 517.1 mn. Foreign investors became net buyers for the first time in eleven weeks with a net buying position of USD 0.6 mn, from a net selling position of USD 7.2 mn recorded the previous week, taking the YTD foreign net selling position to USD 78.4 mn, compared to a net selling position of USD 92.9 mn recorded in 2025.

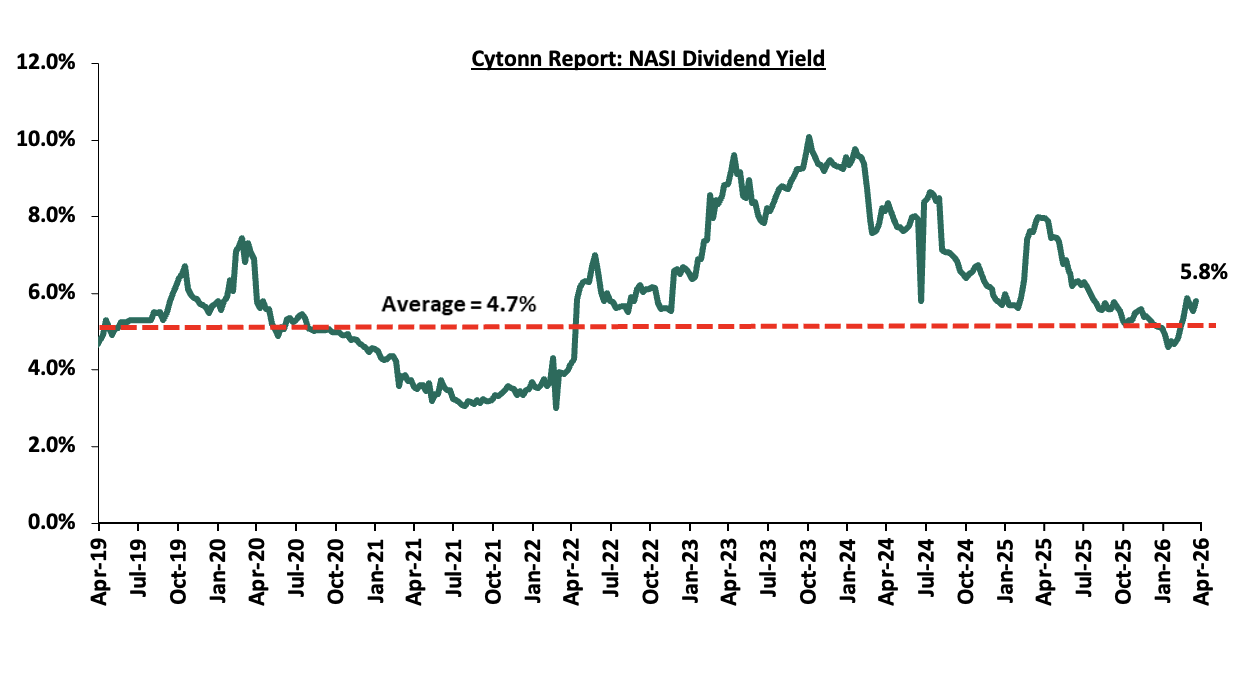

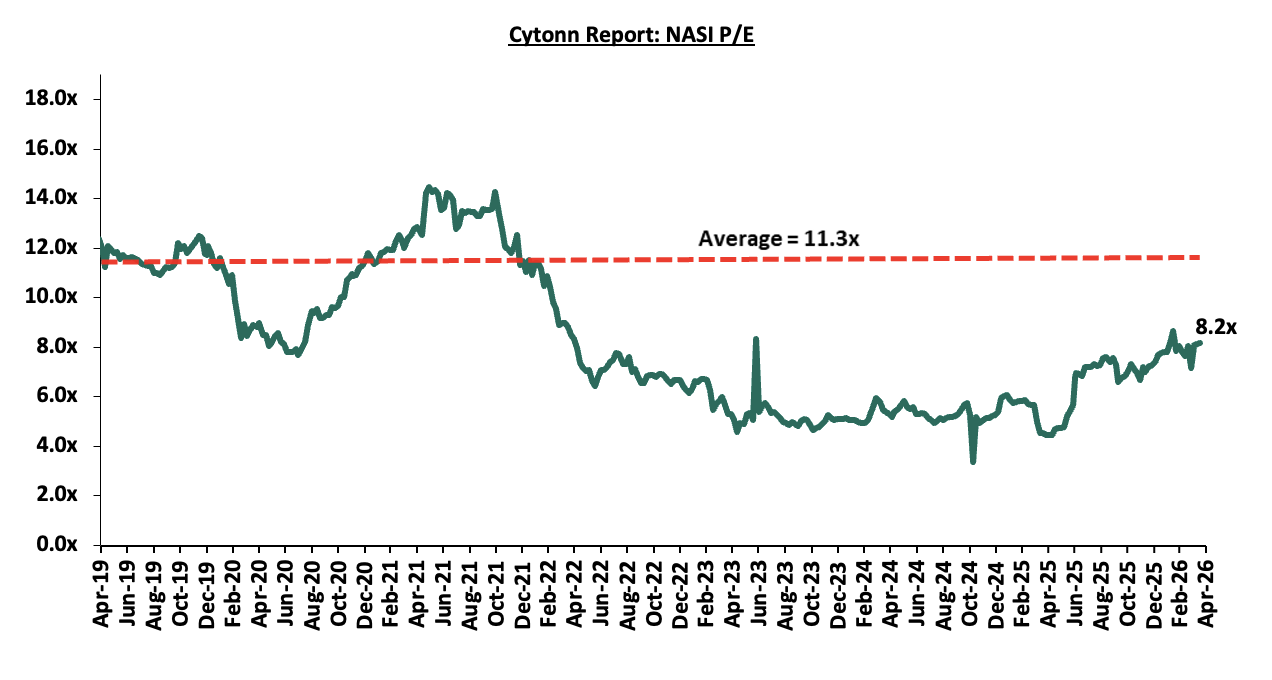

The market is currently trading at a price to earnings ratio (P/E) of 8.2x, 3.1% points below the historical average of 11.3x. The dividend yield stands at 5.8%, 1.1% points above the historical average of 4.7%. Key to note, NASI’s PEG ratio currently stands at 1.0x, suggesting that the market is fairly valued relative to its expected earnings growth. A PEG ratio greater than 1.0x indicates the market may be overvalued while a PEG ratio less than 1.0x indicates that the market is undervalued.

The charts below indicate the historical P/E and dividend yields of the market.

Universe of Coverage:

|

Cytonn Report: Equities Universe of Coverage |

||||||||||

|

Company |

Price as at 10/04/2026 |

Price as at 17/04/2026 |

w/w change |

YTD Change |

Year Open 2026 |

Target Price* |

Dividend Yield |

Upside/ Downside** |

P/TBv Multiple |

Recommendation |

|

KCB Group |

71.0 |

69.3 |

(2.5%) |

5.3% |

65.8 |

81.1 |

10.1% |

27.2% |

0.7x |

Buy |

|

Equity Group |

74.3 |

75.0 |

1.0% |

11.9% |

67.0 |

87.8 |

7.7% |

24.7% |

1.0x |

Buy |

|

I&M Group |

51.5 |

48.5 |

(5.9%) |

13.2% |

42.8 |

56.7 |

7.7% |

24.7% |

0.7x |

Buy |

|

NCBA |

90.0 |

89.8 |

(0.3%) |

5.6% |

85.0 |

103.3 |

7.9% |

23.0% |

1.2x |

Buy |

|

Diamond Trust Bank |

150.8 |

149.8 |

(0.7%) |

30.5% |

114.8 |

175.1 |

6.0% |

22.9% |

0.4x |

Buy |

|

Co-op Bank |

30.9 |

32.5 |

5.2% |

36.0% |

23.9 |

37.2 |

7.7% |

22.1% |

1.2x |

Buy |

|

CIC Group |

4.7 |

4.7 |

(0.9%) |

2.6% |

4.5 |

5.5 |

2.8% |

20.8% |

1.2x |

Buy |

|

Britam |

12.1 |

12.3 |

1.7% |

35.2% |

9.1 |

13.5 |

0.0% |

10.2% |

0.9x |

Accumulate |

|

Jubilee Holdings |

390.0 |

385.8 |

(1.1%) |

19.6% |

322.5 |

407.5 |

3.9% |

9.5% |

0.5x |

Hold |

|

ABSA Bank |

30.9 |

31.5 |

1.8% |

26.6% |

24.9 |

31.7 |

6.5% |

7.4% |

1.7x |

Hold |

|

Standard Chartered Bank |

343.8 |

360.0 |

4.7% |

20.1% |

299.8 |

346.8 |

8.6% |

4.9% |

2.2x |

Lighten |

|

Stanbic Holdings |

280.5 |

289.0 |

3.0% |

46.1% |

197.8 |

273.5 |

7.7% |

2.4% |

1.6x |

Lighten |

|

*Target Price as per Cytonn Analyst estimates **Upside/ (Downside) is adjusted for Dividend Yield *Dividend Yield is calculated using FY’2025 Dividends |

||||||||||

We maintain a “cautiously optimistic” short-term outlook supported the attractive valuations, lower yields on short-term government papers and expected global and local economic recovery, and, “neutral” in the long term as persistent foreign investor outflows continue to constrain market liquidity and limit broad-based market re-rating. With the market currently trading at par to its future growth (PEG Ratio at 1.0x), where performance will be driven by company-specific fundamentals rather than general market direction, we believe that investors should reposition towards value stocks exhibiting strong earnings growth, attractive dividend yields, solid balance sheets, sustainable competitive advantages and trading at compelling discounts to their intrinsic value. While foreign investor sell-offs are expected to continue exerting pressure in the near term, we believe this will create selective entry opportunities for long-term investors.

- Infrastructure Sector

a). World Bank Approved Kshs. 71.0 bn for Mandera Road Upgrade

During the week, the World Bank approved Kshs 71.0 bn (USD 550.0 mn) in financing the upgrade of the Nairobi–Mandera road corridor, marking a significant infrastructure investment under the Horn of Africa Gateway Development Project. The funding will be disbursed in two tranches, including USD 290.0 mn for the additional financing phase and USD 260.0 mn for the second phase of the program. The project targets the upgrade of approximately 508.0 km of the Isiolo–Mandera corridor, alongside the installation of about 1,270 km of high-capacity fibre optic infrastructure, aimed at enhancing both transport and digital connectivity in northern Kenya.

The development underscores a continued policy focus on improving infrastructure in historically underserved regions, with the road upgrade expected to significantly reduce travel time, lower transportation costs, and enhance regional integration with neighboring countries such as Ethiopia and Somalia. The inclusion of fibre optic infrastructure also signals a dual investment approach, combining physical and digital connectivity to unlock economic potential, facilitate trade, and support service delivery in the region. This aligns with broader efforts to position northern Kenya as a key trade and logistics corridor within the Horn of Africa.

Going forward, the upgrade is expected to reduce the journey from Nairobi to Mandera from 3 days to 1-day, lower transport costs which will improve the movement of goods. Better infrastructure is expected to support businesses, government services and cross-border trade.

b.) Nairobi set for Kshs 672.0 mn Greening Initiative

During the week, the Government, in partnership with UNEP and UN Habitat announced Nairobi as the focus of a new Kshs 672.0mn urban greening initiative aimed at transforming parts of the city into greener and more climate-resilient spaces. The programme is expected to target areas including Kamukunji as a pilot “green neighborhood,” with plans to improve urban environmental conditions and public spaces for residents.

The initiative, supported by partners including UNEP, UN-Habitat, and the Government of Kenya, is designed to promote urban sustainability through interventions such as the expansion of green spaces, restoration of urban ecosystems, improved waste management systems, and enhanced climate adaptation measures. The project is positioned as a multi-year effort to reshape how urban development and environmental planning are integrated within Nairobi.

Going forward, the initiative is expected to influence how urban development is approached in Nairobi by placing greater emphasis on sustainability within city planning and infrastructure design. For the real estate and construction sector, we expect an increasingly shaped development requirement, particularly around environmental compliance, green building standards, and integration of public green spaces into future urban project.

- Residential Sector

- Court halts disputed affordable housing project

During the week, the High Court halted the construction of a disputed affordable housing project in Githunguri, Kiambu County, following a legal challenge over the development of 2,180 housing units on the site. The ruling stopped ongoing works as the matter awaits full determination by the court.

The dispute arises from strong opposition by petitioners who argue that the government’s plan to construct 2,180 affordable housing units on the land is inappropriate. They insist that the site should instead be preserved as a national heritage area, raising concerns over land use and historical protection, which ultimately led to the suspension of construction activities. The land is said to have been a historical site where the Mau Mau freedom fighters were executed during colonial era, making it a national heritage land.

Kenya has a housing deficit of 2.0 mn units, with annual demand at 250,000 units to address this, the government targets delivering 200,000 housing units per year under the programme. The suspension of the 2,180-unit Githunguri project therefore slightly reduces annual delivery in absolute terms.

Going forward, the suspension is expected to delay the rollout of the planned 2,180 affordable housing units, creating uncertainty around housing supply delivery from the affected project. It also highlights a growing risk factor for the sector, where land disputes, particularly those involving heritage claims, could slow down implementation timelines and increase legal scrutiny on future affordable housing developments in contested areas.

- Hospitality Sector

- Britam and Ascott in Nairobi Hotel Deal

During the week, Singapore-based lodging operator The Ascott Limited announced a partnership with Kenyan insurer Britam Holdings to develop a new 160-room hotel in Nairobi’s Kilimani area. The project, branded Citadines Westview Nairobi, will be located adjacent to the existing Somerset Westview Nairobi serviced apartments and is scheduled to open in early 2028. The development is structured as a dual-brand hospitality offering targeting both short-stay and extended-stay guests, and is expected to include hotel rooms, studios, and one-bedroom apartments.

The project will also feature supporting amenities such as food and beverage outlets, meeting and conferencing facilities, a swimming pool, and a gym. According to the developers, the hotel is designed to serve both corporate and leisure travellers while tapping into rising demand for professionally managed accommodation in Nairobi. The partnership combines Britam’s real estate investment capacity with Ascott’s global hotel operating expertise, positioning the development within a broader strategy to expand hospitality offerings in key urban centres.

Going forward, the project is expected to strengthen Nairobi’s position as a regional hospitality and business hub as new international hotel supply enters the market. With completion targeted for 2028, It may also encourage further entry of international operators into the market, increasing competition and raising standards in professionally managed accommodation.

- Real Estate Investments Trusts

- Laptrust Imara I-REIT FY’2025 financial report

During the week, Laptrust released the FY’2025 financial results for the Imara I-REIT for the period ended 31st December 2025. The I-REIT holds several properties across the country including; Pension towers, CPF House, Metro Park, Freedom Heights mall, Freedom Heights serviced plot, Man apartments, and Nova Pioneer in Eldoret.

The basic earnings per unit came in at Kshs (0.8) in FY’2025, a 37.2% decline from Kshs (0.6) recorded in FY’2024. The performance was driven by a 37.2% increase in net losses to Kshs 280.3 mn in FY’2025 from Kshs 204.3 mn recorded in FY’2024.

Key points to note from the performance include:

- The basic earnings per unit came in at Kshs (0.8) in FY’2025, a 37.2% decline from Kshs (0.6) recorded in FY’2024. The performance was driven by a 37.2% increase in net losses to Kshs 280.3 mn in FY’2025 from Kshs 204.3 mn recorded in FY’2024,

- Rental and related income for the REIT stood at Kshs 290.6 mn in FY’2025, a 39.3% decrease from Kshs 479.1 mn in FY’2024

- Total operating expenses in FY’2025 for the REIT came in at Kshs 263.3 mn, 11.2% lower than the Kshs 296.6 mn recorded in FY’2024,

- Total assets for the REIT stood at Kshs 6.3 bn in FY’2025, a 5.7% decrease from Kshs 6.7 bn recorded in FY’2024

- Total liabilities in FY’2025 came in at Kshs 0.4 bn, recording a 43.0% increase from Kshs 0.3 bn in FY’2024 wholly attributable to an increase in trade and other payables,

- The shareholder’s funds decreased by 7.7% to Kshs 6.0 bn from Kshs 6.5 bn in FY’2024, mainly attributable to 72.4% increase in revaluation reserve to Kshs 1.3 bn from Kshs 0.8 bn in FY’2024, which outpaced the 15.3% increase in retained earnings to Kshs 314.7 mn from Kshs 272.9 mn in FY’2024

- The REIT currently has a Return on Asset and a Return on Equity of negative (4.4%) and (4.7%) respectively.

Going forward, we expect the expiry of the three-year trading restriction period in 2026 to mark a key inflection point for the I-REIT, as pricing transitions from a net asset value (NAV)-based model to a market-driven mechanism. However, the REIT’s weak operational performance, characterized by declining rental income, compressed yields, and negative returns, may weigh on investor sentiment and result in units trading at a discount to NAV once price discovery sets in.

- REITs Weekly Performance

On the Unquoted Securities Platform Acorn D-REIT and I-REIT traded at Kshs 27.4 and Kshs 23.2per unit, respectively, as per the last updated data on 10th April 2026. The performance represented a 33.4% and 14.5% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. The volumes traded for the D-REIT and I-REIT came in at 13.4 mn and 42.2 mn shares, respectively. Additionally, ILAM Fahari I-REIT traded at Kshs 13.8 per share as of 10th April 2026, representing a 31.0% loss from the Kshs 20.0 inception price. The volume traded to date came in at 1.2 mn shares for the I-REIT, REITs offer various benefits, such as tax exemptions, diversified portfolios, and stable long-term profits. However, the ongoing decline in the performance of Kenyan REITs and the restructuring of their business portfolios are hindering significant previous investments. Additional general challenges include:

- Insufficient understanding of the investment instrument among investors leading to a slower uptake of REIT products,

- Lengthy approval processes for REIT creation,

- High minimum capital requirements of Kshs 100.0 mn for REIT trustees compared to Kshs 10.0 mn for pension funds Trustees, essentially limiting the licensed REIT Trustee to banks only

- The rigidity of choice between either a D-REIT or and I-REIT forces managers to form two REITs, rather than having one Hybrid REIT that can allocate between development and income earning properties

- Limiting the type of legal entity that can form a REIT to only a trust company, as opposed to allowing other entities such as partnerships, and companies,

- We need to give time before REITS are required to list – they would be allowed to stay private for a few years before the requirement to list given that not all companies maybe comfortable with listing on day one, and,

- Minimum subscription amounts or offer parcels set at Kshs 0.1 mn for D-REITs and Kshs 5.0 mn for restricted I-REITs. The significant capital requirements still make REITs relatively inaccessible to smaller retail investors compared to other investment vehicles like unit trusts or government bonds, all of which continue to limit the performance of Kenyan REITs.

We expect the performance of Kenya’s Real Estate sector to remain resilient, supported by several factors: i) World Bank approving Kshs 71.0bn for the upgrade of Mandera road, ii) Nairobi set as as the focus of a new Kshs 672 mn urban greening initiative, iii) Britam-Ascott partnership to develop a new 160-room hotel in Nairobi’s Kilimani area. However, challenges such as slowedmdown affordable housing project in Githunguri, Kiambu county, and the weak investor appetite in listed REITs like ILAM Fahari I-REIT and high capital requirements will continue to constrain the sector’s optimal performance.

Following the release of the FY’2025 results by Kenyan listed banks, the Cytonn Financial Services Research Team undertook an analysis on the financial performance of the listed banks and identified the key factors that shaped the performance of the sector. For the earnings notes of the various banks, click the links below:

- Equity Group FY’2025 Earnings Note

- KCB Group FY’2025 Earnings Note

- Standard Chartered Bank Kenya FY’2025 Earnings Note

- ABSA Bank Kenya FY’2025 Earnings Note

- NCBA Group FY’2025 Earnings Note

- Co-operative Bank FY’2025 Earnings Note

- Stanbic Holdings FY’2025 Earnings Note

- I&M Group Holdings FY’2025 Earnings Note

- Diamond Trust Bank Kenya FY’2025 Earnings Note

- HF Group FY’2025 Earnings Note

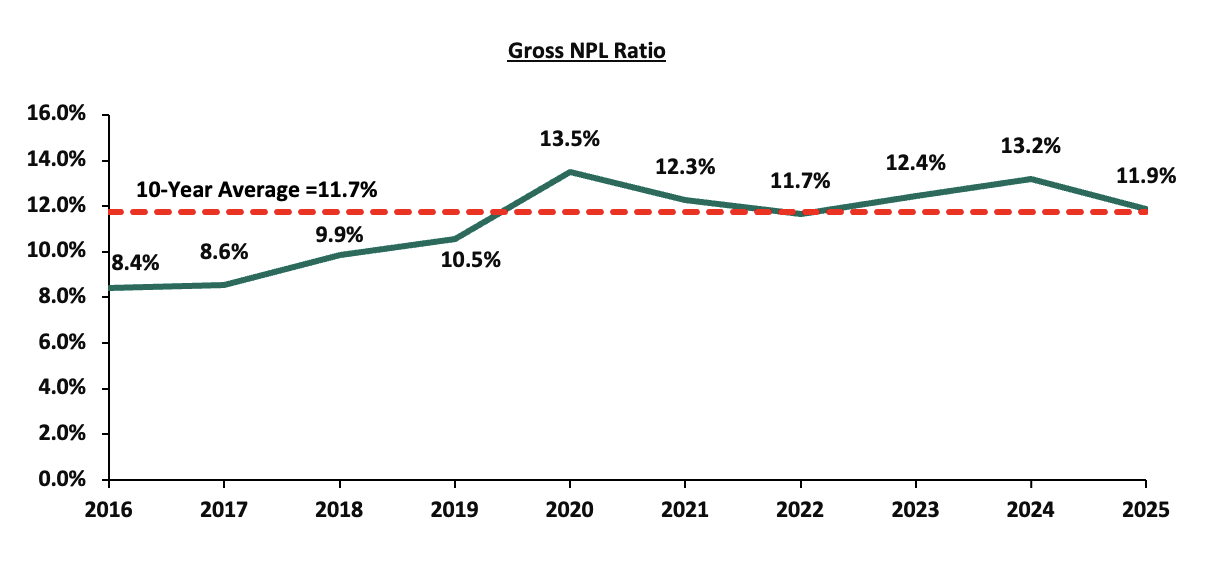

The core earnings per share (EPS) for the listed banks recorded a weighted growth of 15.1% in FY’2025, compared to a weighted growth of 25.7% recorded in FY’2024, an indication of deteriorated performance mainly on the back of a 1.9% growth in non-funded income in FY’2025, compared to a growth of 12.2% in FY’2024. The slowdown reflects muted growth across key NFI components, notably fees and commissions on loans in an easing interest rate environment following CBK rate cuts, alongside lower foreign exchange income due to reduced dollar demand and subdued transaction volumes, highlighting banks’ reliance on interest income. Notably, the inflation rate in FY’2025 averaged 4.1%, 0.4% points lower than the 4.5% average in FY’2024, with the Kenyan Shilling remaining stable against the US Dollar, gaining by 0.2% in FY’2025, to close the year at Kshs 129.0 from the Kshs 129.3 recorded at the beginning of the year. Similarly, credit risk decreased with the asset quality of listed banks improving slightly in FY’2025, with the weighted average Gross Non-Performing Loan ratio (NPL) decreasing by 1.3% points to 11.9%, from 13.2% recorded in FY’2024. The NPL performance remained 0.2% points above the ten-year average of 11.7%.

The report is themed “Earnings Growth Moderates, with Improving Asset Quality and Credit Recovery” where we assess the key factors that influenced the performance of the banking sector in FY’2025, the key trends, the challenges banks faced, and areas that will be crucial for growth and stability of the banking sector going forward. As such, we shall address the following:

- Key Themes that Shaped the Banking Sector Performance in FY’2025,

- Summary of the Performance of the Listed Banking Sector in FY’2025,

- The Focus Areas of the Banking Sector Players Going Forward, and,

- Brief Summary and Ranking of the Listed Banks based on the outcome of our analysis

Section I: Key Themes That Shaped the Banking Sector Performance in FY’2025

In this section, we will highlight the main factors influencing the banking sector in FY’2025. These include regulation, digitization, interest rates, regional expansion through mergers and acquisitions, and asset quality:

- Regulation:

- Risk-based Lending: Over the years, the government has deployed various policy tools to manage interest rates and improve private sector access to credit. Following the repeal of the Interest Rate Cap Law in 2019, the Central Bank of Kenya (CBK) directed banks to adopt risk-based lending models that price loans according to borrower risk profiles, improving fairness and transparency for MSMEs. Although the CBK introduced a revised pricing framework in August 2025 anchored on the Kenya Shilling Overnight Interbank Average (KESONIA), a benchmark derived from actual overnight interbank transactions meant to replace the Central Bank Rate (CBR) for shilling-denominated variable loans, most commercial banks have opted to continue using the CBR as their reference rate under the new model. Institutions such as KCB, Equity, Absa, NCBA, DTB, Stanbic applied CBR plus a customer-specific risk premium since 1st December 2025, despite having previously rejected CBR as a benchmark and championed the creation of KESONIA. Banks cited ongoing systems testing and the need for operational readiness as the reason for delaying adoption of KESONIA, whose higher volatility would also require more frequent lending-rate adjustments and additional regulatory approvals. Co-operative Bank and Kingdom Bank were the first banks to adopt the interbank-based rate. CBK continues publishing KESONIA, currently marginally higher than the 8.75% CBR by 0.15 bps. The revised banking sector Risk-Based Credit Pricing Model (RBCPM) was fully implemented in March 2026. Overall, although the revised framework is intended to strengthen monetary policy transmission, align Kenya with global benchmarks such as SOFR and SONIA, and enhance transparency through mandatory disclosure of lending rates, premiums, and fees, its impact will vary: borrowers with strong credit profiles may benefit from more competitive pricing, while higher-risk customers could face steeper charges, and lending rates are likely to become more responsive, but also more volatile, once full adoption of KESONIA eventually takes effect.

- Higher capital requirements: Following the enactment of the Business Laws (Amendment) Act, 2024, the Central Bank of Kenya (CBK) increased the minimum core capital requirement for commercial banks to Kshs 10.0 bn from the previous Kshs 1.0 bn, which had been in effect since 2012. The new framework requires lenders to comply gradually, Kshs 5.0 bn by 2026, Kshs 6.0 bn by 2027, Kshs 8.0 bn by 2028, and full compliance at Kshs 10.0 bn by 2029. As of December 2025, 6 banks were below the Kshs 3.0 bn threshold and needed a combined Kshs 9.4 bn to meet the December 2025 deadline. The table below shows the core capital requirement gap of the ten banks as of December 2025;

|

Cytonn Report: Selected Banks Core Capital Requirement Gap |

|||

|

No |

Bank |

Core Capital (Kshs Bn) |

December 2025 Gap (Kshs Bn) |

|

1 |

Consolidated Bank of Kenya |

(0.5) |

3.5 |

|

2 |

UBA Kenya Bank |

1.9 |

1.1 |

|

3 |

Access Bank Kenya |

1.1 |

1.9 |

|

4 |

Credit Bank Plc* |

1.2 |

1.8 |

|

5 |

Development Bank of Kenya |

2.2 |

0.8 |

|

6 |

ABC Bank Kenya |

2.7 |

0.3 |

|

Total |

|

9.4 |

|

source: Company Financials, *as of September 2025

The table below shows the core capital requirement gap of the ten banks by December 2026;

|

Cytonn Report: Selected Banks Core Capital Requirement Gap |

|||

|

No |

Bank |

Core Capital (Kshs Bn) |

December 2026 Gap (Kshs Bn) |

|

1 |

Consolidated Bank |

(0.5) |

5.5 |

|

2 |

Credit Bank* |

1.2 |

3.8 |

|

3 |

Access Bank Kenya |

1.1 |

4.9 |

|

4 |

UBA Kenya |

1.9 |

3.1 |

|

5 |

Development of Kenya |

2.2 |

2.8 |

|

6 |

ABC Bank Kenya |

2.7 |

2.3 |

|

7 |

Commercial International Bank |

3.1 |

1.9 |

|

8 |

Middle East Bank |

3.1 |

1.9 |

|

9 |

M Oriental Bank |

3.1 |

1.9 |

|

10 |

Premier Bank |

3.1 |

1.9 |

|

11 |

Bank of Africa |

3.5 |

1.5 |

|

12 |

Guardian Bank |

3.6 |

1.4 |

|

13 |

DIB Bank |

3.7 |

1.3 |

|

14 |

Habib Bank AG Zurich |

3.8 |

1.2 |

|

15 |

Kingdom Bank |

4.9 |

0.1 |

|

Total |

35.5 |

||

source: Company Financials as of December 2025, *as of September 2025

By December 2026, banks will be required to meet the minimum threshold of a core capital of Kshs 5.0 bn. Currently, 15 banks are yet to meet the threshold, and need a combined Kshs 35.5 bn to meet the deadline. Consolidated Bank remains the most distressed, with a negative core capital of Kshs 546.1 mn, requiring over Kshs 5.5 bn to meet the 2026 minimum amid ongoing plans for a rights issue and long-delayed government support. Although the Kenya Bankers Association (KBA) did not expect significant merger and acquisition activity in 2025, arguing that most banks could meet the Kshs 3.0 bn threshold individually, it anticipated heightened consolidation pressure from 2026 onward as capital requirements rise to Kshs 5.0 bn and beyond. In 2026, Paramount Bank has led early consolidation activity with the acquisition of its 100% stake by Nigeria’s Zenith Bank. CBK is currently reviewing the submitted capital plans and monitoring ongoing efforts as banks race to achieve compliance ahead of the phased deadlines.

- Lifting of moratorium on licensing of new commercial banks: In a significant policy shift, the Central Bank of Kenya (CBK) lifted the moratorium on licensing new commercial banks on July 1, 2025, ending a restriction that had been in place since November 2015. The moratorium had been introduced to address governance, risk management, and operational weaknesses in the sector, providing space for reforms. Over the past decade, the industry has undergone substantial strengthening, with improvements in legal and regulatory frameworks, a wave of mergers and acquisitions, and the entry of new strategic investors. With the moratorium now lifted, early indications point to renewed investor interest, particularly from regional financial groups and non-bank financial institutions seeking to upgrade to full banking licenses. While no large-scale greenfield entries have yet materialized, the policy shift is expected to stimulate competition, product innovation, and capital inflows over the coming year, especially as potential entrants assess compliance with the revised minimum core capital requirement of Kshs 10.0 bn. In the near term, the move is likely to deepen financial sector resilience and broaden consumer choice, although the pace of new licensing is expected to remain measured as CBK maintains a cautious, risk-based approval approach.

- Digitization: In FY’2025, digitization continued to be a transformative force in the banking sector, significantly improving how banks operate and deliver services. There has been a significant increase in the adoption of mobile and online banking platforms as customers now prefer to perform banking transactions from the comfort of their homes, leading to a decline in the use of physical branches. For instance, most of the listed banks disclosed that the majority of transactions were conducted through alternative channels, with Equity Group and KCB Group reporting that 4% and 99.0% of their transactions, respectively, were done digitally through non-branch channels in FY’2025,

- Interest Rates: Interest rates were on a downward trajectory during the period under review. Notably, the yields on Kenyan government securities declined during the period under review, with the yield on the 91-day paper averaging 8.3% during the period, 6.9% points lower than the average of 15.2% in FY’2024. The significant declines in rates in FY’2025 led to a decrease in the listed bank’s interest income growth, softening to a weighted average drop of 3.8% in FY’2025, from a weighted average growth of 21.1% in FY’2024. However, the lower interest rate environment led to a substantial reduction in interest expense which declined by a weighted average of 24.9% in FY’2025, compared to the 43.6% growth in FY’2024 this decline in funding cost helped support overall profitability contributing to a 10.8% growth in net interest income in FY’2025,

- Regional Expansion through Mergers and Acquisitions: Kenyan banks are increasingly expanding their regional footprint, with subsidiaries contributing significantly to overall profitability. For instance, Equity Group reported that regional subsidiaries contributed 51.0% of the Group’s Profit Before Tax (PBT) in FY’2025, up from 50.0% in the same period last year, demonstrating the continued importance of these subsidiaries to the Group’s earnings. Additionally, KCB Group’s subsidiaries contributed 29.1% of the Group’s Profit After Tax (PAT) in FY’2025. In terms of consolidation activity, 2025 saw one confirmed acquisition agreement between Access Bank Plc and KCB Group for the acquisition of National Bank of Kenya. More recently, Nedbank announced the intention of acquisition of 66.0% NCBA Group’s shareholding to diversify its regional presence into East Africa.

- On March 19,2026, the Central Bank of Kenya announced the acquisition of 100.0% shareholding of Paramount Bank Ltd by Zenith Bank Plc. The deal was first announced in November 2025, however, the transaction values and details were not disclosed. The acquisition is a strategic entry point into Kenya’s established banking ecosystem, enhancing its geographic diversification and positioning it to tap into Kenya’s relatively mature and dynamic banking sector as a gateway to the broader region. Zenith bank joins other Nigerian banks in the Kenyan market including Access Bank, UBA and GTBank.

- On January 21, 2026, Nedbank announced the intention to acquire approximately 1.1 bn ordinary shares, representing 66.0% of NCBA’s issued share capital, from NCBA shareholders through a partial tender offer, subject to regulatory approvals. The acquisition will be made at a par value of Kshs 5.0 per share, resulting to a total transaction value of Kshs 5.4 bn. If successfully completed, the transaction will result in Nedbank acquiring a controlling interest in NCBA, while the remaining 34.0% of the shares will remain listed on the Nairobi Securities Exchange (NSE). The planned acquisition values NCBA at a multiple of 1.4x its book value. This proposed transaction is part of Nedbank’s stated strategy to extend its reach beyond Southern Africa, prioritizing the high-growth markets of East Africa, especially with Kenya's prominent role as a financial center, bolstered by robust institutions, advanced capital markets and a dynamic technology sector.

- On November 4, 2025 KCB Group Plc revealed its acquisition of an undisclosed minority stake in Pesapal Limited, one of the region’s leading digital payment providers, as part of its strategic initiative to bolster digital capabilities and reinforce its footprint in banking, agency solutions, and business services across Kenya, Uganda, and Rwanda. This move proves to be strategic as KCB strives to capture the biggest market share of the fast-growing fintech market.

- On March 24, 2025, KCB Group Plc disclosed its acquisition of a 75.0% controlling interest in Riverbank Solutions Limited, a fintech entity focused on payment systems, as part of its strategic initiative to bolster digital capabilities and reinforce its footprint in banking, agency solutions, and business services across Kenya, Uganda, and Rwanda. Riverbank, a collaborator with KCB since 2013 in agency banking, brings expertise in digital payments, payroll management, and financial reporting, which KCB aims to harness to enhance its offerings tailored for small and medium enterprises (SMEs) and micro, small, and medium enterprises (MSMEs). The integration of Riverbank’s capabilities is expected to facilitate the unification of KCB’s agent banking channels into a single platform, optimizing operational efficiency.

- On April 14, 2025, the Central Bank of Kenya announced the acquisition of 100.0% shareholding of National Bank of Kenya Limited (NBK) by Access Bank Plc from KCB Group Plc, following CBK’s approval on April 4, 2025 under Section 13 (4) of the Banking Act, and approval by the Cabinet Secretary for the National Treasury and Economic Planning on April 10, 2025, pursuant to Section 9 of the Banking Act. As part of the transaction, CBK, on April 4, 2025, further approved the transfer of certain assets and liabilities of National Bank of Kenya Limited to KCB Bank Kenya Limited pursuant to Section 9 of the Banking Act. The acquisition and completion of the transaction was finalised on 30th May 2025 in accordance with the terms of the Agreement between the parties.

- On March 20, 2024 Access Bank Plc announced that it had entered into a share purchase agreement with KCB Group Plc that would allow Access Bank Plc to acquire 100% shareholding in National Bank of Kenya Limited (NBK) from KCB. Access Bank Plc is a wholly owned subsidiary of Access Holdings Plc listed on the Nigerian Exchange as Access Corporation. Notably, KCB Bank had acquired the National Bank of Kenya back in 2019 in a rescue deal that was supervised by the Central Bank of Kenya. The announcement followed the release of the Q1’2024 results for the KCB group, which revealed a decline in earnings with its Core earnings per share (EPS) declining by 8.3% to Kshs 11.7, from Kshs 12.7 in FY’2022. The transaction represents an important milestone for Access Bank as it moves closer to the achievement of its five-year strategic plan through increased scale in the Kenyan market. In the signed deal, Access Bank will pay multiples of 1.3x the book value of NBK, which stood at Kshs 10.6 bn as of end December 2023. This values the deal at about Kshs 13.3 bn with the actual figure to be announced when the transaction is completed.

The following are Mergers and Acquisitions that were completed in 2024:

- In April 2024, Sidian Bank disclosed that the founders of the bank and other nine individual shareholders relinquished a combined stake of 728,525 shares representing 16.6% stake to Pioneer General Insurance Limited, pioneer Life Investments Limited, Wizro Enterprises Limited, Afrah Limited, and Telesec Africa Limited. The transaction amounted to Kshs 0.8 bn translating to a price to book multiple (p/bv) of 1.0x. This follows an earlier transaction executed on October 2023 when Pioneer General Insurance, Wizpro Enterprise and Afram Limited bought 38.9% stake in the lender following a shareholders’ resolution passed on 20th September 2023 approving the sale,

Below is a summary of the deals in the last 13 years that have either happened, been announced or expected to be concluded:

|

Cytonn Report: Banking Sector Deals and Acquisitions |

||||||

|

Acquirer |

Bank Acquired |

Book Value at Acquisition (Kshs bn) |

Transaction Stake |

Transaction Value (Kshs bn) |

P/Bv Multiple |

Date |

|

Zenith Bank |

Paramount Bank |

Unknown |

100.0% |

Undisclosed |

N/A |

Apr-26 |

|

Nedbank |

NCBA |

6.0 |

66.0% |

5.4 |

1.4x |

Jan-26 |

|

KCB |

Pesapal |

Unknown |

Undisclosed |

Undisclosed |

N/A |

Nov-25 |

|

KCB |

Riverbank |

Unknown |

75.0% |

2.0 |

N/A |

Mar-25 |

|

Access Bank PLC (Nigeria) |

National Bank of Kenya |

10.6 |

100.00% |

13.3 |

1.3x |

Apr-25 |

|

Pioneer General Insurance and four other companies |

Sidian Bank |

5.0 |

16.57% |

0.8 |

1.0x |

Apr-24 |

|

Pioneer General Insurance and two other companies |

Sidian Bank |

5.0 |

38.91% |

2.0 |

1.0x |

Oct-23 |

|

Equity Group |

Cogebanque PLC ltd |

5.7 |

91.13% |

6.7 |

1.3x |

Dec-23 |

|

Shorecap III |

Credit Bank Plc |

3.6 |

20.00% |

0.7 |

1.0x |

Jun-23 |

|

Premier Bank Limited |

First Community Bank |

2.8 |

62.50% |

Undisclosed |

N/A |

Mar-23 |

|

KCB Group PLC |

Trust Merchant Bank (TMB) |

12.4 |

85.00% |

15.7 |

1.5x |

Dec-22 |

|

Equity Group |

Spire Bank |

Unknown |

Undisclosed |

Undisclosed |

N/A |

Sep-22* |

|

Access Bank PLC (Nigeria)* |

Sidian Bank |

4.9 |

83.40% |

4.3 |

1.1x |

June-22* |

|

KCB Group |

Banque Populaire du Rwanda |

5.3 |

100.00% |

5.6 |

1.1x |

Aug-21 |

|

I&M Holdings PLC |

Orient Bank Limited Uganda |

3.3 |

90.00% |

3.6 |

1.1x |

Apr-21 |

|

KCB Group** |

ABC Tanzania |

Unknown |

100.00% |

0.8 |

0.4x |

Nov-20* |

|

Co-operative Bank |

Jamii Bora Bank |

3.4 |

90.00% |

1 |

0.3x |

Aug-20 |

|

Commercial International Bank |

Mayfair Bank Limited |

1.0 |

51.00% |

Undisclosed |

N/A |

May-20* |

|

Access Bank PLC (Nigeria) |

Transnational Bank PLC. |

1.9 |

100.00% |

1.4 |

0.7x |

Feb-20* |

|

Equity Group ** |

Banque Commerciale Du Congo |

8.9 |

66.50% |

10.3 |

1.2x |

Nov-19* |

|

KCB Group |

National Bank of Kenya |

7.0 |

100.00% |

6.6 |

0.9x |

Sep-19 |

|

CBA Group |

NIC Group |

33.5 |

53%.47% |

23 |

0.7x |

Sep-19 |

|

Oiko Credit** |

Credit Bank |

3.0 |

22.80% |

1 |

1.5x |

Aug-19 |

|

CBA Group** |

Jamii Bora Bank |

3.4 |

100.00% |

1.4 |

0.4x |

Jan-19 |

|

AfricInvest Azure |

Prime Bank |

21.2 |

24.20% |

5.1 |

1.0x |

Jan-18 |

|

KCB Group |

Imperial Bank |

Unknown |

Undisclosed |

Undisclosed |

N/A |

Dec-18 |

|

SBM Bank Kenya |

Chase Bank Ltd |

Unknown |

75.00% |

Undisclosed |

N/A |

Aug-18 |

|

DTBK |

Habib Bank Kenya |

2.4 |

100.00% |

1.8 |

0.8x |

Mar-17 |

|

SBM Holdings |

Fidelity Commercial Bank |

1.8 |

100.00% |

2.8 |

1.6x |

Nov-16 |

|

M Bank |

Oriental Commercial Bank |

1.8 |

51.00% |

1.3 |

1.4x |

Jun-16 |

|

I&M Holdings |

Giro Commercial Bank |

3.0 |

100.00% |

5 |

1.7x |

Jun-16 |

|

Mwalimu SACCO |

Equatorial Commercial Bank |

1.2 |

75.00% |

2.6 |

2.3x |

Mar-15 |

|

Centum |

K-Rep Bank |

2.1 |

66.00% |

2.5 |

1.8x |

Jul-14 |

|

GT Bank |

Fina Bank Group |

3.9 |

70.00% |

8.6 |

3.2x |

Nov-13 |

|

Average |

|

|

74.5% |

|

1.3x |

|

|

Average: 2013 to 2018 |

|

|

73.5% |

|

1.7x |

|

|

Average: 2019 to 2026 |

|

|

73.2% |

|

1.0x |

|

|

* Announcement Date ** Deals that were dropped |

||||||

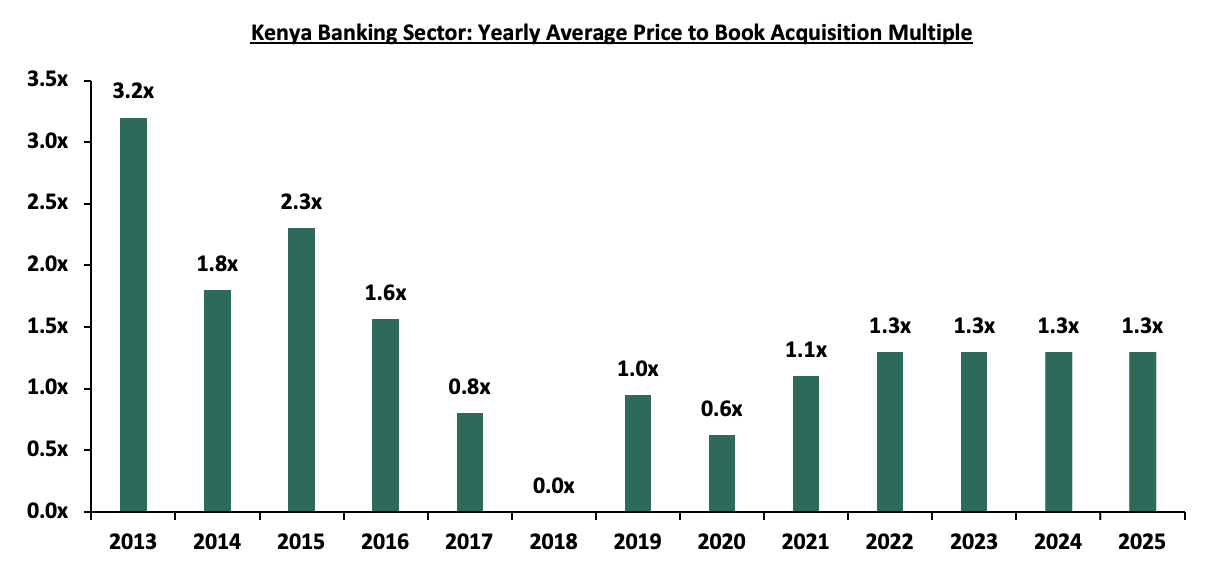

In 2025, the average acquisition valuations for banks have remained unchanged at 1.3x, similar to what was recorded in a similar period in 2024. As such, the valuations still remain low compared to historical prices paid, as highlighted in the chart below;

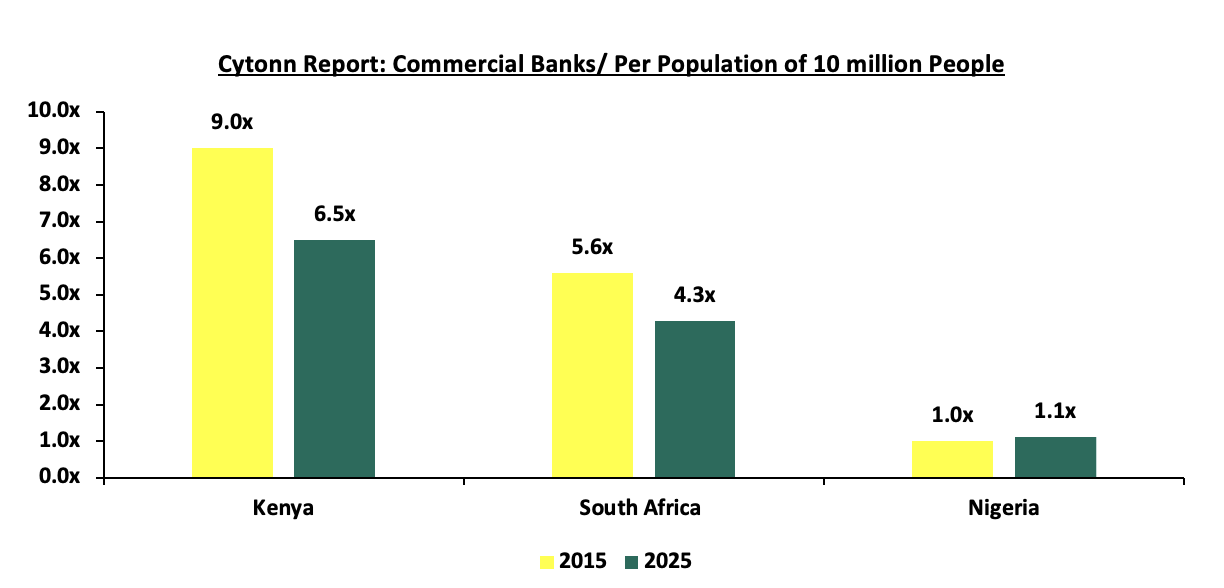

As at the end of FY’2025, the number of commercial banks in Kenya stood at 38, same as in FY’2024, but lower than the 43 licensed banks in FY’2015. The ratio of the number of banks per 10 million population in Kenya now stands at 6.5x, which is a reduction from 9.0x in FY’2015, demonstrating continued consolidation in the banking sector. However, despite the ratio improving, Kenya still remains overbanked as the number of banks remains relatively high compared to the African major economies. To bring the ratio to 5.6x, we ought to reduce the number of banks from the current 38 banks to about 33 banks. This is partly expected to be supported by the enactment of The Business Laws (Amendment) Act 2024 that mandated a significant increase in the minimum core capital for banks to Kshs 10.0 bn from the previous Kshs 1.0 bn that had been in effect since 2012. To facilitate compliance, lenders below this threshold were directed to incrementally grow the figure over a 5-year period, required to close 2025 with a minimum core capital of Kshs 3.0 bn, rising to Kshs 5.0 bn by the end of 2026, and full compliance at Kshs 10.0 bn by the end of 2029. The new capital requirement is likely to trigger further mergers and acquisitions (M&As), especially for smaller lenders that may struggle to meet the threshold, potentially reducing the number of banks even further. However, the effect could be muted by the lifting of the moratorium which ended on 1st July 2025. The chart below shows the commercial bank ratio per 10 million people across select African nations in comparison to Kenya;

Source: World Bank, Central Bank of Kenya, South Africa Reserve Bank, Central Bank of Nigeria

The Central Bank of Kenya (CBK) ended its moratorium on licensing new commercial banks, effective July 1, 2025, a restriction that had been in place since November 2015 to support sector reforms. During the moratorium period, the banking sector strengthened through improved regulatory frameworks, greater consolidation, and the entry of strategic investors, with the number of banks declining to 38 from 43 in 2015. With the restriction lifted, new entrants can now apply for greenfield banking licenses, provided they meet the revised minimum core capital requirement of Kshs 10.0 billion. This shift reduces dependence on mergers and acquisitions as the main entry route and opens up direct market entry under stricter capital requirements.

- Asset Quality: Asset quality for listed banks improved in FY’2025, with the weighted average Gross Non-Performing Loan ratio (NPL) decreasing by 1.3% points to 11.9%, from 13.2% recorded in FY’2024. The performance remained 1.2% points above the ten-year average of 11.7%. Notably, all the 10 listed banks recorded a decrease in their NPL ratios, signalling an improvement in asset quality even as credit risk remains elevated compared to historical levels, albeit showing signs of moderation following recent monetary policy easing and improving lending conditions. Similarly, most banks experienced a decline in gross non-performing loans coupled with growth in gross loans. As a result, the overall gross non-performing loans (NPL) ratio in the banking industry decreased by 1.5% points, falling to 15.4% in December 2025 from 16.9% in September 2025. Additionally, KCB Group’s NPL ratio declined the most by 3.7% points to 16.2%, from 19.8% in FY’2024, while HF Group’s NPL ratio decreased by 3.1% points to 22.2%, from 25.3% in FY’2024. KCB’s asset quality improved due to a 0% increase in gross loans to Kshs 1,308.3 bn, from Kshs 1,137.2 bn recorded in FY ‘2024 compared to the 6.1% decrease in Gross non-performing loans to Kshs 211.8 bn, from Kshs 225.7 bn in FY’2024. Similarly, HF Group’s asset quality improved due to a 5.3% growth in gross loans to Kshs 49.8 bn from Kshs 47.3 bn in FY’2024, compared to the 7.5% decline in gross non-performing loans to Kshs 11.1 bn from Kshs 12.0 bn in FY’2024. The chart below highlights the asset quality trend for the listed banks:

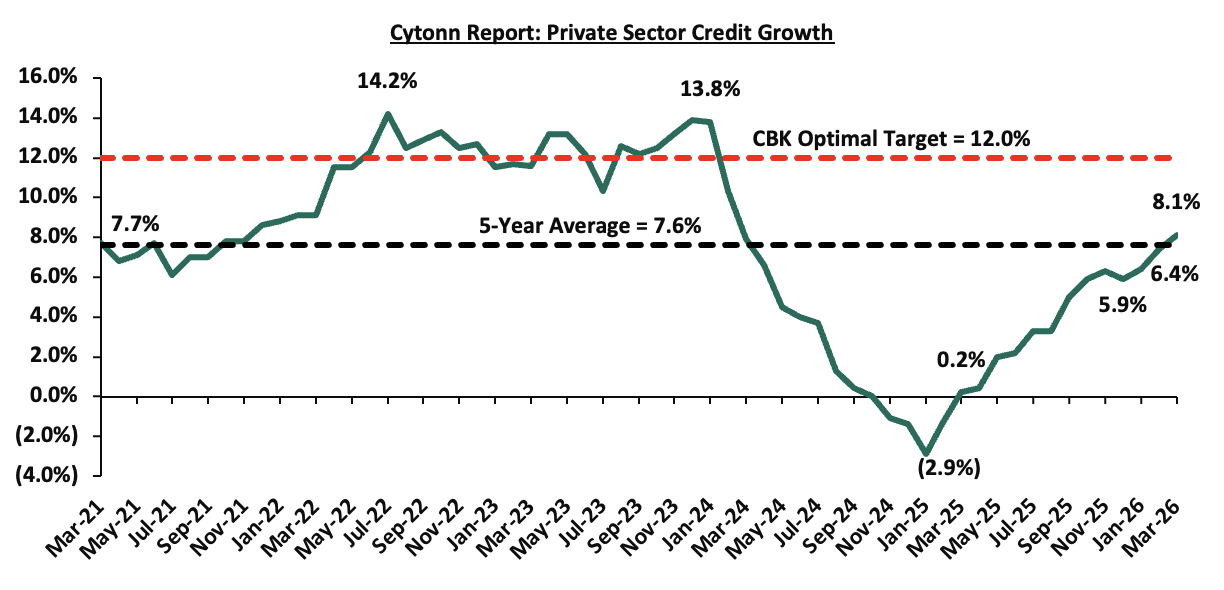

All the ten listed Kenyan banks recorded an improvement in asset quality, supported by enhanced credit risk management and early signs of economic recovery as the recent Central Bank Rate (CBR) cuts began to filter through the economy. In a bid to curb inflation and support the Shilling the Monetary Policy Committee (MPC) had adopted an accommodative monetary policy stance, lowering the Central Bank Rate (CBR) to 9.00% in December 2025 compared to 11.25% in December 2024. With commercial banks required to reflect these lower rates in their loan pricing, the banks weighted average lending rates therefore declined by 2.1% points to 14.8% in December 2025 from 16.8% in December 2025. As a result of the low interest rates, the private sector credit growth improved recording expansions of 5.9% in December 2025 and further to 8.1% in March 2026, up from a contraction of 1.4% in December 2024. The chart below shows the private sector credit growth:

The Central Bank of Kenya has lowered the Central Bank Rate (CBR) by a cumulative 425 basis points, from 13.0% in July 2024 to 8.75% in February 2026, signalling a gradual easing of monetary policy following the successful stabilization of the currency and anchoring of inflation. However, in the April 2026 meeting, the MPC maintained the CBR rate at 8.75% pausing the easing, to anchor inflation expectations within the 2.5%–7.5% target band while also supporting exchange rate stability. The Committee further highlighted that rising global oil prices, driven largely by geopolitical tensions in the Middle East, present upside inflation risks through potential second-round effects.