Apr 5, 2020

During Q1’2020, the United Nations Economic Commission for Africa (UNECA) released the World Economic Situation and Prospects for 2020, revising the Sub-Saharan Africa (SSA) GDP growth to 1.8% from the earlier projected 3.2% in January 2020. The lower growth rate was majorly attributed to the economic impact of the COVID-19 pandemic set to disrupt supply chains, plummeting commodity prices and key sectors such as tourism, agriculture, oil and mining set to be greatly affected. The projections for 2020 are lower by 140 bps compared to the previous projection of October 2019, which stood at 3.4%. The largest economy in SSA, Nigeria, is expected to experience a less robust GDP growth in 2020 with the International Monetary Fund (IMF) revising this downwards by 30 bps to 2.0%, from 2.3% previously, attributable to the decline in the oil price growth and disruption of global supply chains due to the COVID-19 pandemic.

Currency Performance

All select currencies depreciated against the US Dollar except for the Ghanaian Cedi, which remains unchanged supported by market reforms which included the rate at which the commercial banks were willing to commit to exchange the currency for the USD at a future rate. The depreciation recorded by the currencies is partly attributable to the ongoing COVID-19 pandemic, which has seen a fast-falling demand for export commodities particularly from China, the most vital trading partner and the epicenter of COVID-19 outbreak. The Zambian Kwacha was the worst performer, depreciating by 22.3% against the dollar YTD owing to the low economic productivity with the fall of copper prices and drought, compounded with heavy imports which continue to put pressure on the local currency. The Kenya Shilling depreciated by 3.6% to close the quarter at Kshs. 105.1 against the US Dollar attributable to demand from merchandise importers who had entered contracts before the coronavirus-related disruptions, buying hard currency to offset them in the current thin market with very little dollar inflows, prompting the Central Bank of Kenya (CBK) to sell dollars, despite their earlier plan to purchase dollars from the market to improve forex reserves. Below is a table showing the performance of select African currencies:

|

Select Sub Saharan Africa Currency Performance vs USD |

|||||

|

Currency |

Mar-19 |

Dec-19 |

Mar-20 |

Last 12 Months change (%) |

YTD change (%) |

|

Ghanaian Cedi |

5.4 |

5.7 |

5.7 |

(5.3%) |

0.0% |

|

Malawian Kwacha |

724.5 |

729.1 |

729.3 |

(0.66%) |

(0.03%) |

|

Tanzanian Shilling |

2315.5 |

2293.0 |

2308.0 |

0.3% |

(0.6%) |

|

Ugandan Shilling |

3714.9 |

3660.0 |

3785.0 |

(1.9%) |

(3.3%) |

|

Kenyan Shilling |

100.7 |

101.3 |

105.1 |

(4.2%) |

(3.6%) |

|

Mauritius Rupee |

34.9 |

36.2 |

39.1 |

(10.7%) |

(7.4%) |

|

Botswana Pula |

10.8 |

10.5 |

12.0 |

(9.7%) |

(12.2%) |

|

Nigerian Naira |

361.0 |

306.0 |

360.0 |

0.3% |

(15.0%) |

|

South African Rand |

14.5 |

14.0 |

17.8 |

(18.7%) |

(21.5%) |

|

Zambian Kwacha |

12.2 |

14.1 |

18.1 |

(32.8%) |

(22.3%) |

African Eurobonds:

Yields on African Eurobonds increased in Q1’2020 after a decline in 2019. This was partly attributed to the COVID-19 health crisis, with investors attaching a higher risk premium on the affected regions due to the anticipation of slower economic growth.

During the quarter, the Government of Ghana, on 4th February 2020 issued the longest dated Eurobond as part of debt issuance to raise USD.3.0 bn. The government launched the sale of a USD 750.0 mn tranche, which will amortize and have an average life of 40-years at a yield of 8.9%. The bond was oversubscribed 5x to USD 14.0 bn indicating a huge interest for Ghana's debt.

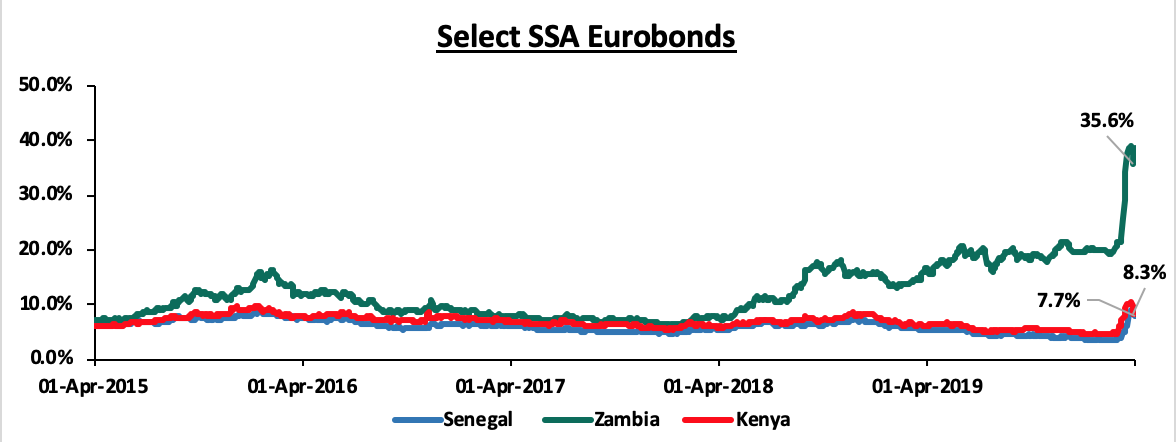

Below is a graph showing the Eurobond secondary market performance of select 10-year Eurobonds issued by the respective countries:

Analysis of trends observed in the chart above is as follows:

- Yields on the Zambia Eurobond increased in Q1’2020 by 19.1% points as a result of a mass exodus of foreign investors amid fears of the country’s debt sustainability and the ongoing COVID-19 pandemic, with most investors believing it to be close to default. Yields on its USD 750.0 mn of notes due in September 2022 soared 14.7% points to 66.3% attributable to the weakening copper prices and drought, which has led to power cuts caused by low water levels at its hydroelectric dams. Credit rating companies including Fitch Ratings had already warned of a high risk of default even before copper prices fell 20.0% this year as the coronavirus pandemic disrupts markets. Zambia’s currency is the world’s worst performer this year, and foreign-exchange reserves have fallen to a record low and cover less than two months of imports. The country intends to implement liability management of its external debt portfolio to lengthen maturity and enhance its capacity to meet debt-service obligations.

- Yields on Kenyan and Senegalese Eurobonds have been increasing since the beginning of the year, signaling that the demand for the instruments has declined during the period. The trend was replicated in all the Eurobonds attributable to the expected economic decline due to the COVID-19 pandemic. Emerging market bond funds have also endured heavy net outflows as investors have dumped risky assets amid the deepening coronavirus crisis. Outflows from Emerging Markets debt funds hit USD 17.0 bn in the seven days to March 25, 2020. The past four weeks have seen a total of USD 47.7bn withdrawn from the sector, equivalent to 10.2% of assets under management. The exodus has so far erased a third of the USD 140.0 bn of net inflows that Emerging Markets bonds have seen in the past four years, according to Bank of America.

Equities Market Performance

Most of the Sub-Saharan African (SSA) stock markets recorded negative returns in Q1’2020. The region experienced capital outflows, a downgrade from last year’s recorded inflows. This is attributable to the ongoing Coronavirus pandemic, with investors selling out of the equities market in favor of safe havens and the expected economic fallout. Below is a summary of the performance of key exchanges:

|

Equities Market Performance (Dollarized*) |

|||||

|

Country |

Mar-19 |

Dec-19 |

Mar-20 |

Last 12 Months change (%) |

YTD change (%) |

|

Rwanda |

0.1 |

0.1 |

0.2 |

60.0% |

14.3% |

|

Tanzania |

0.9 |

1.5 |

1.5 |

67.8% |

0.7% |

|

Ghana |

458.8 |

405.5 |

378.9 |

(17.4%) |

(6.6%) |

|

Kenya |

1.5 |

1.6 |

1.3 |

(16.0%) |

(21.3%) |

|

Zambia |

460.5 |

303.3 |

233.3 |

(49.3%) |

(23.1%) |

|

Uganda |

0.5 |

0.5 |

0.3 |

(32.0%) |

(32.0%) |

|

Nigeria |

85.4 |

87.7 |

59.2 |

(30.7%) |

(32.5%) |

|

South Africa |

3866.2 |

4079.3 |

2493.8 |

(35.5%) |

(38.9%) |

|

*The index values are dollarized for ease of comparison |

|||||

Analysis of trends observed in the chart above is as follows:

- Rwanda is the best performing index showing resilience amid the COVID-19 pandemic following gains made by cross-listed stocks such as Equity Bank, which has recorded YTD gains of 25.7%,

- South Africa recorded the worst performing index with losses of 38.9% attributable to the continued selloffs brought by concerns about the economic fallout caused by the Coronavirus, despite assurances that the cabinet is putting together an economic stimulus package to deal with the detrimental impact from the actions taken to combat the virus,

- The performance of the Nairobi All Share Index (NASI) was driven by losses of 21.3%, YTD attributable to the ongoing Coronavirus pandemic, with investors selling out of the equities market.

GDP growth in Sub-Saharan Africa region is expected to decline owing to the ongoing COVID-19 pandemic that is expected to disrupt global supply chains and as the currencies lose value against the dollar in an uncertain global economy. Key risks remain difficult business conditions and poor infrastructure, reliance on commodity exports, political tension in some countries and debt sustainability due to high levels of public debt in most economies in the region. Stock market valuations remain unattractive for long-term investors.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma